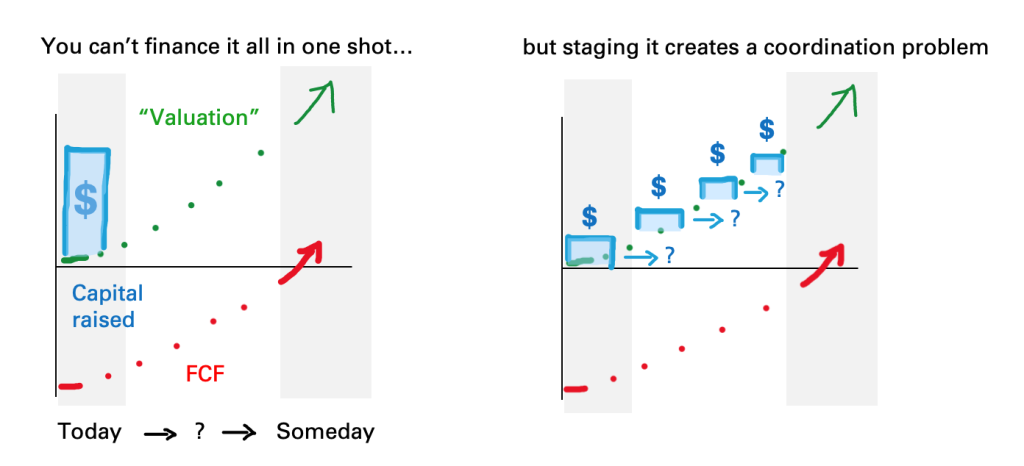

The role of startup valuation in staged capital deployment

In his article VCs should play bridge, Alex Danco described the Capital Coordination problem in venture capital, created by the staged nature of investments.

I recommend reading the whole piece, but the summary is that investments are de-risked by staging capital over future milestones (with the implied valuation step-ups) rather than investing everything up-front and hoping for the best.

The heart of this strategy is the signalling game where investors offer affirmation of the investment for their capital partners.

“This gives the next investor cover to say, ok, I’ll do the same thing. I’ll invest at $20M, sending a signal: I believe that this price reflects a discount to the next round. This 20 million price, by current convention, means we believe this hand will play out as another X million in GMV run rate”, or whatever it is your signalling for this new round of bidding.”

Danco’s assessment speaks to the oddly myopic perspective of “venture math“: investors are primarily focused on understanding incremental progress (measured with ARR) rather than the ultimate outcome. This has come at a cost to sectors that are slower to start generating revenue but solve much more important problems.

He’s right to frame venture capital as collaborative (Bridge) rather than strictly adversarial (Poker), this also highlights issues like enmeshment and collusion which emerge when so much stress is put on relationship-driven outcomes over objective measurement.

The approach that Danco describes as “convention bidding” is framed as an alternative to the zero-sum attitude of formal valuation — where investors are primarily concerned with securing their own returns rather than participating in affirmative semaphore.

Indeed, this reflects a revealed preference for market signals over conviction which should trouble anyone who still believes venture capital is responsible for risk capital formation.

Discounting the Future

Peter Thiel on the importance of pitching your startup as a “discount to the future”

Most founders will pitch their startup valuation as a sort of premium on the last round (e.g. “Our valuation last year was X, we’ve made Y progress, and now we deserve a valuation 2x greater.”)… pic.twitter.com/WZ0fSHxWhH

Further to the above, Danco’s article is a good reflection of venture capital’s poor grasp of valuation, characterised by three common misconceptions:

Valuation is transient, and at each stage a new valuation would need to be calculated — creating uncertainty that threatens signal-driven coordination.

Valuation is the same as price, and entry points are more a function of market norms and comps than they are of fundamental value creation.

The practice of valuation is built on too much uncertainty to be practical for early stage companies.

While the first is inaccurate, the second is actually dangerous. The general practice of market-driven pricing has created huge structural fragility in venture capital, exacerbating the already painfully boom-and-bust nature.

The third, however, is just silly. All investments are predicated on valuation, at least in theory (the alternative being mindless momentum investing). The only difference is whether it’s written out with explicit assumptions or a mental calculation with implicit assumptions.

Indeed, valuation is essentially the story of a startup (“What happens if things go right?”) translated into numbers, with some discounting for the cost of capital and risk of failure. You can think of it as the financial source code of a pitch.

Usefully, by calculating a terminal value based on that story and discounting it using the expected rate of return in venture capital, you can also ascertain a healthy entry point for future rounds — assuming the startup remains broadly on track.

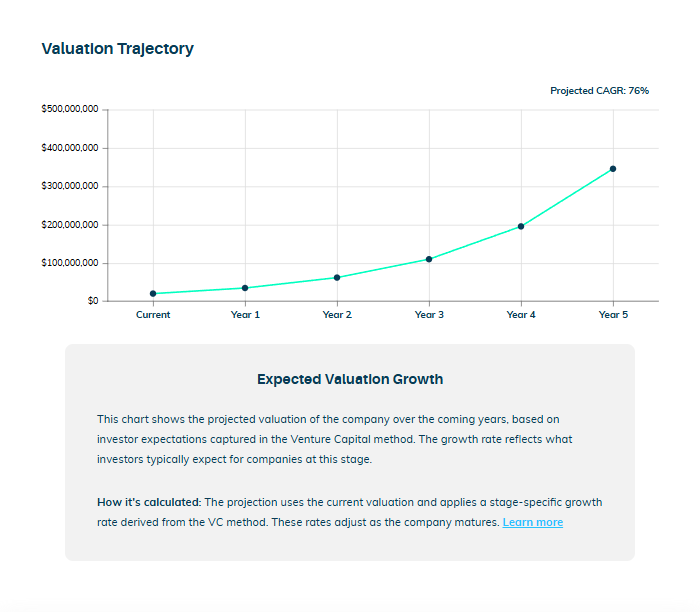

Consider the below: the valuation of a Seed round, calculated on Equidam at just over $20M. As a part of this calculation, and the future it’s predicated on, you can also see the valuation trajectory for the forecasted period. If the company raised a Series A at ~30 months, the valuation would be around $85M.

Of course, all of the usual caveats: the future is uncertain, startups pivot, markets shift. However, it’s fairly easy to built those adjustments into a model and see how they change both today’s valuation and the future trajectory.

Assessing valuation with a higher resolution view of performance enables better judgements: Perhaps top-line revenue is growing on track, but costs are surging. Maybe revenue is lagging, but margins are way better than expected.

The hope is not that forecasts play out precisely, but that they give you a useful relative perspective on performance over time.

If venture capitalists wanted a way to coordinate staged capital in the future, to finance a company efficiently (with minimal time spent agonising over terms) while ensuring a good risk-adjusted return for all investors, this is the logical approach.

Valuation is essentially the process of aligning expectations across market participants by transparently exploring data and assumptions. Typically this occurs between buyer and seller (VC and founder) in a specific transaction, but there’s no reason why downstream capital providers couldn’t benefit from that work.

It also offers the vital benefits of helping investors better understand the value of novel innovation, and limiting exposure to systematic risk of market-based pricing — getting caught in the trap of “money chasing deals“.

(top image: “The Bulls and Bears in the Market” by William Holbrook Beard)

Whether you’re investing in mature companies in the public market, or fast-growing startups in the private market, one question separates good and bad investors:

Do you understand valuation?

Valuation is the rationale by which you determine which opportunities to pursue. To develop your understanding of valuation is to develop your ability to recognise potential.

Despite the central role in investment decisions, valuation is often misconstrued as financial engineering or market-driven pricing exercises.

Valuation is an opinion

Here’s three things valuation is not:

Based on verifiable inputs

Provably accurate in output

A mirror of market sentiment

Instead, valuation is always an opinion based on a set of assumptions about an unknowable future.

“People act like it’s an award for past behavior. It’s not. It’s a hurdle for future behavior.”

Whether that valuation is based on a detailed DCF model or napkin-math, it’s an opinion. And it’s no more or less of an opinion as your process gets more or less sophisticated; the only difference is how clearly you outline the assumptions.

When one investor states that a company is overpriced, and another that it is undervalued, neither is right or wrong in the moment — they just have differing opinions.

Valuation can be a simple, implicit part of the process, or it can be an explicit exercise used to better understand an opportunity and check assumptions.

Valuation is a story about the future

In order to form an opinion about a particular future, you must first listen to its story.

“The value of a stock is what people believe it is and could be. A stock is a story.”

Valuation is the art of using stories to develop opinions about the future

Valuation can be broken down into a few pieces:

How do you judge the credibility of a story?

How do you estimate the economic potential of a story?

How do you estimate the risk associated with a story?

You can think about this via two extremes:

You’re looking at a company you’re familiar with. You’ve got a good mental model of the industry, the technology, the market forces, trajectory, and risks. It’s relatively simple for you to make a rough judgement on value in your head. This reflects Kahneman’s “System 1” thinking.

You’re looking at a company you have no familiarity with. The technology is novel, the market is emerging, and there’s no real precedent. In order to make a good judgement, you have to submerge yourself in details and scenarios. This reflects Kahneman’s “System 2” thinking.

In the latter case, a more sophisticated valuation process can help you understand the credibility and economic potential of a story. It provides a framework for ingesting information that can control biases, while allowing you to recognise and scrutinise the main drivers of value.

Valuation is essentially the act of running simulations of the future described in a story, focused on the numbers rather than the narrative, to explore the potential.

Pricing is not valuation / Trading is not investing / The present is not the future

Venture capitalists often choose to focus on relative pricing, instead of valuation, as an attempt to proxy experience through crowdsourced activity — allowing for speedy “System 1” style investment decisions.

This means analysing industry activity, which biases investment towards categories with low information friction like B2B SaaS, at a cost to sectors with more idiosyncracy, like deeptech.

Unfortunately that focus on market data also means these investors are not developing their ability to make judgements about the future, only to pattern match today. This compounds into a ‘knowledge worker atrophy‘ problem, weakening venture capital’s institutional competence at funding creative endeavors and novel solutions.

That would appear to be a critically weak link in the value proposition of venture capital, and the premise that it funds important solutions to humanity’s problems.

Consider this simple truth: All value created from Series A to exit is downstream of the first check. Without initial belief, the foundation of VC collapses.

This relatively thin slice of venture (by capital) is therefore disproportionately important. All future returns are directly attributable to the industry’s ability to surface new opportunities.

Despite this fundamental importance, venture capital is structurally rigged against origination:

Origination is inherently a small check pursuit, as these ideas need minimal capital to validate propositions.

LPs are biased against highly diversified VC strategies, particularly with the growth of Fund of Funds, which makes scaling an origination strategy more challenging.

Thus, origination is the domain of smaller firms, with smaller funds. This runs contrary to the compensation incentives in venture capital, which push successful investors to raise larger funds and invest at later stages.

“In exploring its sources, we document several additional facts: successful outcomes stem in large part from investing in the right places at the right times; VC firms do not persist in their ability to choose the right places and times to invest; but early success does lead to investing in later rounds and in larger syndicates.”

So, in addition to the existing problem of VC’s lack of institutional knowledge and high churn, good investors are often squeezed out of this origination focus if they wish to achieve greater scale.

Origination is the foundation on which all future VC returns are built, yet it is systematically underresourced and underallocated

You should be dubious of any venture capitalist that claims “there’s too much capital, and not enough good opportunities”.

You will never this claim from VCs focused on origination, who have to spend a distracting amount of time on their own fundraising — even when their track record is strong. Again, their size prohibits them from more easily raising from larger institutions.

This chronic misalignment sets the ceiling on what venture capital can achieve in returns and accelerated innovation

Instead, shifting allocation earlier, to improve origination, without any increase in capital, has an effect equivalent to doubling the total capital pool.

If all venture returns are downstream of origination, you would expect that a specific focus on origination would lead to outperformance amongst VCs. You would be right:

“The consensus in recent literature is clear: proactive deal origination is pivotal for achieving superior outcomes in venture capital investments.”

Fundamentally, this issue will not be resolved as long as the incentives in VC mean the primary opportunity is to maximise fee income by optimising for proxy metrics.

There is very little intrinsic motivation for VCs to take excessive career risk on highly idiosyncratic ideas, which generate slower markups than consensus startups, in the hope that they may generate some carry a decade down the line.

In summary: Venture capital is structurally set up to pile capital into categories with low information friction, which is diametrically opposed to innovation.

You’d have to be brave, crazy or stupid to do anything else.

The brilliant exceptions

Fortunately, for everyone involved, there are a few mission-driven firms that have made it their business to focus on origination.

In today’s market, you’re either a lifecycle capital partner to founders, or you’re a niche operator originating unique opportunities for those who can be.

To originate deal flow, one needs some combo of:

– unique networks; – top tier reputation in a niche; or – uncommon levels of investment rigor for company stage

All of these help drive signal for the company, which is incredibly valuable in a noisy market.

They have each developed specific proactive strategies to find high potential opportunities, first — sometimes before there’s even a company to invest in.

Firms that focus on early conviction and speed, like 1517 Fund and Hustle Fund — who write tiny inception checks to help prospective founders take the first step.

Firms that focus on research and expertise, like Compound and Not Boring Capital — who find contrarian needles in consensus haystacks by processing vast quantities of information.

Firms that focus on process and scale, like BoxGroup, Boost VC and First Round — who manage the greater idiosyncratic risk of origination with discipline and portfolio strategy.

Firms that focus on community and talent density, like South Park Commons, and Entrepreneur First — who allow opportunity to manifest from pools of brilliance.

(They all share the key elements: community, research, process and speed.)

It’s hard to state just how much value can be attributed to these firms, and a few others like them. Relative to their size, they are responsible for a disproportionate amount of founder opportunity and downstream potential.

To understand the potential for these models, Y Combinator and Founders Fund are a good illustration of the same principles at scale. For a range of reasons, these two firms have broken out of the orbit of VC’s structural limitations.

To conclude, a quote from Danielle Strachman on 1517 Fund’s approach to origination, and some links to great conversations with the other firms above:

“We call it turning over rocks. It’s like, oh, I went to this campus and I found an interesting young person; we’re turning over rocks. You go to a hackathon and my favorite thing is to look for the young person who is staring off into space. They’re by themselves because they built their own thing. You go up and you talk to them and you’re like, whoa, okay, you are really super nerded-out on security and you’re talking to me like I should know what you’re talking about, and I have no idea. But we’re gonna talk for a while and we’re gonna figure this out.”

Relying on market efficiency while investing in idiosyncrasy

Venture capital is the hunt for outliers; ideas that are not well understood by the wider market. This strategy is rooted in the need for risk capital to finance frontier businesses.

You can see how this played out in previous generations of tech: Amazon, Airbnb, Canva, Coinbase, Dropbox, Google, Shopify, Slack, Uber… All of these companies faced an uphill battle with investor interest, and went on to produce incredible exits for the early believers. Similarly, there are many examples where the founder’s own capital paved the way: SpaceX, Tesla, Palantir, Anduril…

On the other hand, it seems relatively more difficult to find stories of competitive early rounds leading to great outcomes. Stripe, perhaps?

This understanding of venture capital is reinforced by the data:

We find that consensus entrants are less viable, while non-consensus entrants are more likely to prosper. Non-consensus entrepreneurs who buck the trends are most likely to stay in the market, receive funding, and ultimately go public.

Despite this, today’s venture capitalists have an absurd reliance on the market as their lens to understand value. Herd behavior drives investor attention, and (what passes for) valuation is primarily derived from relative measures like ARR multiples.

Investors set out to generate alpha with their unique ability to recognise novel opportunities, but rely on broad market sentiment as a lens to understand what is worth pursuing.

This paradox has stumped observers.

This heavy reliance on comparable companies in the VC valuation process is perhaps unsurprising, given that relative pricing methods are not uncommon in M&A markets overall. What is less clear, however, is the exact driver behind this method, and the understanding of why a relative pricing methodology will impact startups’ valuations.

Whether it’s marketplaces, crypto or today’s AI boom, capital herds into the category and drives up prices, and those prices then become “comps” for others.

Ultimately, the surge in deals creates a greater volume of market data for that category, reducing information friction for investment, allowing for more deals to be made more quickly. This compounding influence quickly overheats activity.

In addition to competition driving up prices and compressing due diligence timelines, there’s a further pernicious consequence: while information friction is reduced around the consensus, it is increased elsewhere.

Founders building truly innovative products find themselves facing a wall of blank-faced investors programmed with category multiples. The difficulty of raising capital becomes so great that many simply reorient their ambition to lower quality projects closer to the experience of venture capitalists. This is clearly a fundamental failure:

Information frictions in valuation can lead startups to select projects that align with the expertise of potential venture capital (VC) investors, a strategy I refer to as catering […] where a startup trades off project quality with the informational benefits of catering.

If all of this was to hold true, we should see an increase in performance by the few VCs that maintain a lens on fundamental (rather than relative) value. In theory, these investors would be better able to recognise outlier value and unique opportunities.

Indeed, that does appear to be the case. Multiple studies on venture capital investment performance and decision making processes have reached the conclusion that VCs would benefit from a better understanding of fundamental value:

Venture capital funds who base their investment strategy on fundamental values and a long-term view seem to have a measurable advantage over those who engage in subjective short-term trading strategies.”

Ideally, a startup would combine a full fledged fundamental cash flow-based approach with a thorough comparable companies analysis to cover both its intrinsic value and a market-based measure.

So, the paradox is laid bare and the remaining question is why this is the case. There are two potential explanations:

VCs do not understand valuation. A decade of ZIRP-fuelled spreadsheet investing has destroyed the institutional understanding of risk and the purpose of venture capital.

There are other incentives at work which explain this phenomenon; reasons why VCs would be reluctant to closely analyse fundamental value.

Explanation 1: Hanlon’s Razor

Unsurprisingly, there’s plenty of evidence to make the case that this is unintentional; a result of simple incompetence and herd behavior. Indeed, herding is a well-studied phenomenon in professional investment, particularly when insecurity is high:

Under certain circumstances, managers simply mimic the investment decisions of other managers, ignoring substantive private information. Although this behavior is inefficient from a social standpoint, it can be rational from the perspective of managers who are concerned about their reputations in the labor market.

Chronic groupthink, and the atrophy of independent reasoning, further explains why VCs are also often unable to clearly articulate the process that goes into their investment decisions:

The findings suggest that VCs are not good at introspecting about their own decision process. […] This lack of systematic understanding impedes learning. VCs cannot make accurate adjustments to their evaluation process if they do not truly understand it. Therefore, VCs may suffer from a systematic bias that impedes the performance of their investment portfolio.

Many VCs have simply emulated the practices of their peers without fully understanding why. Indeed, those peers probably couldn’t provide a rationale either. It’s an industry of investors copying each other’s homework while pretending to be original thinkers.

Action without understanding purpose naturally erodes standards. Not only does this make VCs bad fiduciaries, it also precludes any learning and institutional development.

Almost half of the VCs, particularly the early-stage, IT, and smaller VCs, admit to often making gut investment decisions. We also asked respondents whether they quantitatively analyze their past investment decisions and performance. This is very uncommon, with only one out of ten VCs doing so.

The alternate theory is that there may be some genuine motive for VCs to avoid looking too carefully at fundamental value. That somehow they are able to profit from a reality in which it is not an important driver of activity.

Perhaps it is simply because today’s VCs behave more like traders, rather than investors. That the easier opportunity is to glom onto hot categories and ride the exuberance to an overpriced exit somewhere down the line, rather than trying to find good investments.

This is also not an original accusation:

For those who are holding on to the belief that venture capitalists are the last bastion of smart money, it is time to let go. While there are a few exceptions, venture capitalists for the most part are traders on steroids, riding the momentum train, and being ridden over by it, when it turns.

Venture capital, as a discipline, runs an existential risk of invalidating itself by becoming institutionally what crypto is colloquially. If venture capital is just about “[creating] the impression [of] recoupment”, then its no better than the pump and dumps of the crypto bros.

Yet again, there’s evidence that this is the case.

VCs are heavily influenced by market conditions, optimism and FOMO. None of these are original accusations, although it might be interesting to learn this has been demonstrated in research:

The optimistic market sentiments and fears of missing out in hot markets can significantly shift VCs’ attention towards cheap talk, such as promises of high growth. Such conditions may even prompt VCs to neglect costly signals such as the profitability of new ventures.

This is confirmed by research looking at this question from the other side, where it is demonstrated that VCs are commensurately less likely to herd in periods with greater uncertainty and less optimistic momentum to channel capital:

The study finds a significant negative relationship between economic policy uncertainty (EPU) and herding behavior, indicating that venture capitalists are more likely to make independent judgments when EPU rises.

Even when a VC talks about wanting to find category winners, they are also implicitly talking about riding a category. Were they hunting for genuine outliers, the category wouldn’t matter. There is a reason, for example, why some VCs widely publicise the categories they invest in as great opportunities, and others choose to keep any alpha for themselves.

The final reason is simple: subjective, market-based pricing is opaque and open to manipulation. VCs can collectively produce and support higher marks regardless of underlying value. They can also choose to be “opportunistically optimistic” about a portfolio company:

During fundraising periods the valuations tend to be inflated compared to other periods in the life of the fund. This has large effects on reported interim performance measures that appear in fundraising documents. We find a distinctive pattern of abnormal valuations which matches quite closely the period up to the first close of the follow on fund. It is hard to rationalize the pattern we observe except as a positive bias in valuation during fundraising.

Indeed, much of the fallout post-2022 involved LPs feeling fairly miffed that managers weren’t being honest about underlying portfolio company value. As long as VCs broadly maintained marks, there was still hope to raise another fund on those mostly meaningless proxy metrics of performance.

In Conclusion,

Many VCs choose to play a short-term trading game By focusing on market momentum, rather than companies, through relative valuation methods, VCs operate more like traders.

Most VCs take the path of least resistance when adopting practices While analysing fundamental value offers outperformance, relative value is easier to understand and offers strategic advantages.

Most VCs identify as investors, and some of them still are. Mostly the smaller, boutique firms who were quick to realise that they could not compete in consensus categories against the multi-stage platforms.

There is value in being a trader if you have multi-billion dollar funds and can both manifest and then coast on the beta of technology markets. They behave like market makers on the way up, extracting opportunistic liquidity, and can aim to concentrate resources into the handfull of winners before the market turns.

This strategy is toxic to smaller investors, many of whom are simply washed out in the boom-and-bust cycles that this amplifies. Instead, these investors, focused on identifying true outliers, need to consider polishing their lens on fundamental value.

(top image: Ascending and Descending by M.C. Escher)

The two faces of what we sometimes call venture capital, and the cognitive dissonance they create.

This blog started out as a place to write about the intersection of science fiction and technology. The first article about venture capital, and the opium of consensus, emerged from watching VCs herd into thinly-veiled crypto scams in the name of “web3“.

The influence of consensus remains poorly understood, and the subject of distracting counterfactuals, despite being widely discussed for as long as “investor” has been a profession.

Words must have meaning

Venture capital is the practice of identifying nascent business opportunities with radical potential; the application of process to extract outsized value from extreme idiosyncratic risk.

In this context, venture capital is clearly not a consensus-oriented discipline. Both theoretical and quantitative perspectives support this reality; the intention, goals, behavior and performance.

We find that consensus entrants are less viable, while non-consensus entrants are more likely to prosper. Non-consensus entrepreneurs who buck the trends are most likely to stay in the market, receive funding, and ultimately go public.

Simply look back at the early-days of venture capital’s largest outcomes, where the majority did not have investors competing for access, driving up the price. Fundraising was a struggle for those founders, and in that struggle was the opportunity for those on the other side of the table.

It’s very hard to make money on successful and consensus. Because if something is already consensus then money will have already flooded in and the profit opportunity is gone. And so by definition in venture capital, if you are doing it right, you are continuously investing in things that are non-consensus at the time of investment.

Indeed, if consensus were to play a meaningful role in venture capital, it would fail on the only two things it sets out to achieve:

Maximise ROI for LPs through idiosyncratic risk

Finance the development of novel innovations

In addition, there is no such thing as a downstream supply of “non-consensus capital”. If you fund non-consensus companies then you have to be able to support them to the point where their potential is obvious and larger/later generalists can be convinced. It’s paradoxical to believe that other investors will share your non-consensus viewpoint.

Cognitive dissonance

The root of the confusion about consensus (and entry price, portfolio construction, attention, relationships…) is the mixing of two different private market strategies. One is venture capital, and the other is something else that just falls into the venture capital allocation bucket.

This other strategy emerged in the period from 2011 to 2021, enabled by low interest-rates, as described by Everett Randle in “Playing different games“:

Tiger identified several rules / norms / commonly held ideas in venture/growth that are stale & outdated and built a strategy to exploit the contemporary realities around those ideas at scale.

So you have massive capital allocators looking for places they can farm yield and they don’t want to be slinging hundreds of $30M checks. Capital agglomerators represent the perfect solution. Hit your 7-8% yield target, be able to park $250M a pop without being the majority of the fund, and sit back and relax.

This hunger to capture the most extreme “power law” category leaders is a requirement of the exit math involved in multi-billion dollar funds. Consequently, these platforms also raise substantial early-stage funds to index any emerging theme, putting an option on the future of those companies.

A mega-VC with $5-10B annual funds is really searching for only one thing: a company they can pile over $1b into with a potential for 5-10X on the $1b. With this, seed fund is inconsequential money used to increase the odds of main objective.

The startup industrial complex that has emerged is not optimised for non-consensus investing, and nor does it need to be. Investors at these platforms are hired to compete and win in known areas — and have attitudes to match:

Successful startups fit into a mold that investors understand, and that more often than not those startups attracted meaningful competition among top investors.

If a company has tons of hype and seems overvalued, don’t run away. Run towards it. Hype is good. Means they’ll raise, exit at higher valuation. And the price likely won’t feel overpriced after the startup exits.

The output is a rough index of high-growth private technology companies. The platforms are harvesting the beta from innovation, rather than finding the alpha in outliers. Even the giant outcomes become so well/over-priced that their returns risk converging with benchmarks.

Categorically, this is not venture capital in any meaningful sense.

The only reason we call this venture is because LPs need to call it venture so CIOs can hit annual allocation targets they promised boards. This is venture allocation, not venture returns.

To repeat a point already well-hammered, the platform strategy is entirely different, with a different LP base, a different return profile, and different rules.

The difference between the Andreessen quote above, and the more recent quotes from Chen and Casado, is simply that in 2014 Andreessen Horowitz was a venture capital firm. Today it is an asset manager, an RIA with a multi-stage platform strategy, perhaps best described as a venture bank.

Many VCs have sought to assimilate “tier 1” multi-stage behavior, acting out what they believe LPs and peers expect to see despite the fundamentally incompatible models. This herding around identity and behavior reflects the extreme level of insecurity in venture capital, a product of the long feedback cycles and futility of trying to reproduce success in a world of exceptions.

There is no harmony with venture capital, and the behaviors of these platform investors should not be emulated by venture capitalists — whether or not they also call themselves venture capitalists.

To put a point on this: The platforms explicitly benefit from consensus and price inflation. Both are toxic to venture capital.

As long as both strategies are discussed under the banner of venture capital, we’ll keep wasting time on pointless debates about markets and incentives, and investors will keep making dumb, confused decisions.

(top image: A Steam Hammer at Work, by James Nasmyth)

The influence of productivity shocks, peer effects and cost of capital on AI IPO ambitions, and what happens next.

While leaders at xAI, Anthropic and Mistral have been silent on their plans to go public, OpenAI is starting to open up.

Back in May it was reported that negotiations with Microsoft included provisions that allowed OpenAI to file for an IPO. The transition to a Public Benefit Corporation (PBC) the following month made that technically possible. Both Altman (CEO) and Friar (CFO) have made statements alluding to the process since. Indeed, simply the fact that Friar is being put in front of the media more often as a leadership figure is a significant signal.

OpenAI’s most recent release may underline this direction. By prioritising model economics (focusing on the “router” capability) rather than model performance, the reception to GPT-5 was poor. In reality, this may reflect a shift in posture toward public market metrics, and their willingness to take the PR hit.

The prompt router also lays the groundwork for OpenAI to provide selective access to more expensive models. The next generation of LLMs will be powered by NVIDIA’s Blackwell chips, offering ~30x faster real-time inference. The chips are rolling out at the moment, with an impact on model releases expected next year.

Assuming these models will be a major step-up in competence, this could be the tipping point for a wave of AI IPOs in 2026.

Factor 1: Productivity Shocks

In our model, two firms, with differing productivity levels, compete in an industry with a significant probability of a positive productivity shock. Going public, though costly, not only allows a firm to raise external capital cheaply, but also enables it to grab market share from its private competitors.

When an industry experiences (or anticipates) a significant positive productivity shock (an inflection point in their ability to generate value), this may trigger an “IPO wave”.

Essentially, if there’s a significant step-up across the industry then there’s a real incentive to be the first (or at least be early) to tap public markets for capital to drive market-share expansion.

LLMs have continued to improve over the last few years, with a number of hyped releases and growing experimentation amongst enterprise users, but there has yet to be a truly significant “productivity shock” moment.

Factor 2: Peer Effects

We find that observing a peer go public within the previous 12 months raises the propensity to undertake an IPO from a baseline rate of 0.31 percent per quarter to 0.44 percent per quarter, amounting to a 40 percent increase in IPO propensity. This result is robust to accounting for hot market effects and other common shocks that may affect competing firms’ IPO decisions.

The first to market has an advantage in that they may capture the demand for that industry amongst public market investors. They also bear all of the cost and the risk of blazing that trail, primarily that they might have greatly overestimated demand.

There is some benefit to being a “fast follower” in these circumstances, which is often what triggers the “IPO wave” dynamic seen in the culmination of tech cycles. However, the later you are in that wave, the less of the benefit you capture.

These periods, often characterised as “IPO windows” have been referred to in literature as “windows of misopportunity” for investors due to the increased failure rate. However, it’s also true that the few survivors tend to appear more innovative (in patent quality and quantity) than IPOs issued in other periods.

Overall, this chapter tend to conclude that “windows of opportunity” provides real opportunity to the most inventive private firms and allow them to raise public capitals to further their innovations.

We find that less profitable companies with higher investment needs are more likely to IPO. After going public, these firms increase their investments in both tangible and intangible assets relative to comparable firms that remain private. Importantly, they finance this increased investment not just through equity but also by raising more debt capital and expanding the number of banks they borrow from, suggesting the IPO facilitates their overall ability to raise funds.

There’s a common perception that going public is for mature companies who are past the period of aggressive growth, looking for more stable access to capital. This does not appear to be true.

In fact, companies that IPO are often doing so in order to increase their investment in growth, including intangible assets including R&D spend. This is particularly true in heavily competitive markets and capital-intensive businesses.

This has obvious relevance to LLM providers, who check a lot of these boxes. Certainly, in the phase of investing in infrastructure to support scale, lowering the cost of capital is a major priority.

Factor 4: Beyond Hedging

Similar to going public, hedging mitigates the effect of risk on a firm’s product market strategy, and, thus, results in greater product market aggressiveness. Therefore, in the presence of product market competition, hedging has a strategic benefit similar to that of an IPO. Importantly, we show that the availability of hedging reduces, but does not eliminate, the incentives to go public.

Not necessarily a reason why LMM providers may look to IPO, but rather why they haven’t until now: “Hedging” in this context effectively reflects the relationships that many model providers have with large public companies like Microsoft, Amazon or Apple.

Rather than going public themselves, they can rely on these partnerships to fund investment and distribute risk, offering some of the benefits of going public without any of the costs.

However, the example of OpenAI’s relationship with Microsoft illustrates that it’s possible to outgrow these arrangements.

IPO Windows

Generally speaking, “IPO windows” are a mirage chased by liquidity-starved venture capitalists. A truly great company, like Figma, can IPO more-or-less whenever it wants to.

However, that dynamic changes when you have a group of peer-companies in a fiercely competitive (and capital intensive) industry. At that point, it is likely that there will be some strategic clustering of IPO ambitions.

A true “IPO window”, 1999/2000 or 2021, involves ~1,000 companies listing in the space of about six months. Diligence collapses, the quality of companies goes in the toilet, and public markets are torched for years afterwards. Sarbanes-Oxley killed this behavior in 2002, and it didn’t appear again until the low-interest-rate pandemic briefly drove public markets insane in 2021.

Why Wait

Assume that OpenAI is likely to be the first out. As today’s AI leader, with the widest consumer adoption and biggest brand, it seems the best positioned.1

What are they waiting for?

Primarily, they’ll be waiting to see if Blackwell unlocks the kind of productivity shock they are looking for. To clear their recent $500B valuation they’ll need to go public with undeniable momentum and a great story to tell new investors about future potential.

Secondly, going public is just a huge amount of work. Both in a technical sense, preparing the company’s books for intense scrutiny, and in a brand and PR sense. Prospective investors may need educating about the product, or the image of leadership may need some rehabilitation.2

IPOs are remarkably intense, and represent the most thorough inspection that a company will endure in its lifetime. This is why companies and their board of directors agonize over whether or not they are “ready” to go public. Auditors, bankers, three different sets of lawyers, and let us not forget the S.E.C., spend months and months making sure that every single number is correct, important risks are identified, the accounting is all buttoned up, and the proper controls are in place.

There has been endless talk of a bubble of AI investment, and certainly there seems to be a disconnect between price and value.

This is true in private markets, reflected in transaction data, and in public markets, reflected by the delta between the MAG7 (all somewhat AI-connected) and the other 497 companies in the S&P.

However, the truth is that bubbles only really happen in public markets. They require liquidity, enabling the wild sentiment-driven swings in price that characterise a bubble.

In illiquid markets, like venture capital, you have what William Janeway called “speculative episodes”, which may be derived from a bubble playing out in public markets (via comps) but do not behave in the manner of a bubble.

It’s almost as if wherever there is a liquid trading secondary market in assets, there you will find a bubble.

Indeed, the concept of bubbles has been used in VC to disguise what is better described as simple greed and myopia. Investors behaving like traders — “riding the momentum train, and being ridden over by it, when it turns” — to quote Damodaran.

It’s illogical to describe what is happening today as a bubble if all of the current participants (including Altman himself) acknowledge that it looks like a bubble. A key feature of speculative bubbles is surely that the participants do not realise it’s a bubble? A more honest characterisation is simply that VCs are choosing to gamble on AI because their LPs believe they should.

This all changes when AI companies hit public markets, and the pool of investors (and capital) grows dramatically.

Consider the environment: post productivity shock, with an IPO wave led by the largest model providers but cascading into related industries and any company tha can crest the narrative.

This is precisely, and clasically, when we’d see a bubble emerge; in the volatile public markets, rather than the sluggish and opaque private markets.3

Until then, call it what it is: degenerate trading behavior.

(top image: Allegory on Tulipmania by Jan Brueghel the Younger)

As a minor footnote here, I believe Altman’s recent comments about AI as a bubble, his uncertainty at leading a public company, and an AI CEO in 3 years, are all deliberate narrative prompts. [↩]

This also fits neatly with Howard Mark’s comments about the markets feeling ‘expensive’, and the potential for a major correction in the not-so-distant future. [↩]

In 2014, Mark Schaefer coined the term “Content Shock“, to describe the point at which the amount of content being produced outgrew our available time to consume it. The implication being that a lot of content would be written that would be entirely overlooked.

The upshot: increased spend on SEM and social media platforms, and content that was increasingly designed to grab attention.

A similar phenomenon is happening with startups today, as highlighted by Sam Lessin, in his draft letter to LPs.

A summary of the problem:

Investors can only view so many pitches, so they rely on early signals of competence (pitch quality, MVP, early traction) to filter through opportunties efficiently. Not perfect, but it works.

Today, with AI, it’s easier for anyone to develop a high quality pitch, a slick looking MVP, and even some initial revenue. Some of these are companies that would have emerged without AI, but many are just riding the wave and trying to get lucky.

There’s a narrative violation happening right now that a lot of people aren’t talking about. The AI hype is certainly frothy and those frothy rounds are making the news. But the reality is that most AI companies just don’t get funding…

Some founders see genuine opportunity to do something important with the new technology.

Some see an opportunity to exploit investor enthusiasm to raise a load of money.

With AI, the technology driving the enthusiasm also makes it easier to build a startup. Specifically, that it makes it easier to build a startup that passes a typical VC’s filters.

The outcome is a huge amount of time spent chasing dead ends. Which may or may not involve capital deployed.

Screening for Outliers

This isn’t necessarily a problem at the first stage of screening inbound deals, where it’s relatively easy to select for a two basic truths:

Do we think the problem is important?

Do we think the founders are credible?

Or, in a pragmatic sense, is the startup on a path that seems likely to unlock vast amounts of economic energy?

For an example of how to scale this process, look no further than Y Combinator. For obvious reasons, that organisation has become very good at screening applications in large volume.

A central element to this process is the single slide format which partners use to review applications. It contains much of the information needed to make the judgement mentioned above, but much more importantly it doesn’t include information that may introduce bias.1

This isn’t something you should farm out to associates or agents, and neither should you rely on warm intros for signal.

You just have to do the work™.

Recognising Talent

The hard part begins when you turn your attention to a pool of viable opportunities and need to determine which have real potential.

You can make a judgement on whether you think the problem is important, which reflects on the quality of the founders in the “package deal” nature of pitches.

What you can no longer do as easily is test for founder credibility, given the glossy-finish provided by AI tools. This can be broken down in two main categories:

Do they understand the business model? Acquisition costs, unit economics, procurement timelines, cashflow, customer appetite, margins and moats?

Do they understand the implementation? The physics, transaction costs, regulation, R&D, infrastructure requirements and scalability?

Previously, you could get a good understanding of this from a well-developed pitch deck and an MVP. Today, AI can fill in a lot of those answers for otherwise incompetent or poorly-motivated founders.

One clue for how this problem may be addressed lies in Sam’s letter to LPs:

A generation ago to make an investment VCs would say ‘where is your detailed business plan’. The business plan as an artifact served two purposes for investors; (1) it allowed you to ideally actually know / get up to speed on the business, (2) the form of the business plan and the thinking inside it told you something about how smart / talented / diligent the team was. It was easy for investors to process relative volume of inbound because they could read a few pages of a bad business plan (just like a bad script) and say ‘pass’ vs. ‘oh this person is smart’.

Sam suggests that business plans fell out of favour because (similar to today’s problem) it became easier to build a prototype and put together a nice deck. I’d take that a step further, with some observations learned via Equidam’s 14 years in the business of valuation and fundraising:

The prolonged zero interest-rate period and the surge of SaaS solutions destroyed financial literacy in venture capital. It reduced much of the logic to a simple formula:

CAC: $20

ARR/customer: $4

Net cash: -$16

Multiple: 20x

$1 Invested = $4 in (gross) NAV

For over a decade, all many VCs cared about was how soon cash-incinerating SaaS growth engines could convert capital calls into NAV inflation and enable subsequent funds.

The upshot was that investors, founders, advisors, and accelerators all forgot the basics of finance and economics. Cash flow doesn’t matter that much for SaaS… Projections are just extensions of the typical growth logic, and don’t serve a useful purpose… Theyr’e all just the same assumptions… The atrophy accelerated as capital flowed more freely, with fewer questions asked.

Another (infuriating) consequence was that in a decade of unprecidented investment in venture capital, most of the money was shovelled into recursive NAV inflation, and very little progress was made on important problems in biotech, energy, infrastructure etc.

By way of example, Equidam would have had a MUCH easier time over the last 15 years if it conjured up some bullshit private market multiples to value SaaS companies. Instead, with the mission to help get funding to the best opportunities, it has stuck by a principled and rigorous approach to valuation.

Particularly, this includes using projections properly, and consequently most of what Equidam does is actually teaching founders how to do projections well, and teaching investors how to parse them.

Fortunately, this too can be reduced down to a simple-ish formula:

Is the founder’s pitch coherent and credible?

If so, where do you expect the company to be, financially, in 3-5 years?

Given typical success rates, anticipated dilution, and time to exit, what is the value today?

Essentially, the difference is that this approach looks at the specificfuture of the company in order to understand value, rather than applying a generic multiple to past performance. This is a much more appropriate lens when you’re looking for outliers.

The main criticism from ZIRPers is that the future is too uncertain, and projections are too unreliable. This earns them a blank stare and a strong cup of coffee.

The entire purpose of venture capital is to make well informed, rational judgements about the future. If you aren’t comfortable investing based on assumptions, then one of two things is true:

You should not be working in venture capital.

You don’t understand the assumptions.

(Though perhaps the second point also points to the first.)

This leads to one of the most misunderstood points about valuation, which I’ll try and use to pivot this article towards a conclusion:

Valuation is not intended to determine the right price.

It is an exercise which, when done properly, helps both sides of a transaction understand the assumptions and align their expectations. From that scenario, you get an indication of value which can inform the price you agree on, but the value is in the process itself.

Thus, the key here, and what has been missing from venture capital for more than a decade now, is a return to financial literacy, rather than financialisation.

Sit down with founders. Talk through their strategy together, using both the deck and the financial model as a guide. Connect it with questions about the business and technical implementation. Their answers, guided by your questions, should slot together to create a coherent and credible picture of the future.

Done well, this should give you a huge amount of insight into the founders, and their company.

Indeed, it turns out that founders who go through this process actually have a significantly easier time raising capital. This is one of the many reasons I’m so irate when people tell founders to “let the market price the round”. The process of valuation is so valuable, so useful, and so important to innovation.

So, you’re going to see a lot more startup pitches in your inbox over the next couple of years. It would be a grave mistake to ignore them, so you need to figure out how to embrace this process.

Step 1: Learn from Y Combinator’s process for screening deals. Particularly, learn what not to look at in order to reduce the vectors for bias in your process. Limit as much as possible.2

Step 2: Find a way to dig into this “complete package” of strategy, business model and technical implementation in a way that establishes founder credibility and can’t be faked with AI.

It doesn’t have to be all at once. You can start by asking them to send you a video talking through their financial model and deck to explain the underlying strategy and how it connects to revenue/profit targets and milestones. Eventually, though, it should probably be in-person, where hopefully you can get a sense for their passion and tenacity.

(header image: ‘Deluge’ by Ivan Aivazovsky)

I can see why YC includes traction for their objectives, but I’d argue it’s perhaps a negative to include for a seed fund. i.e. it may bias your review towards companies with traction, rather than the best companies. [↩]

To be honest, I don’t even like that the YC template includes the logo. It seems like unnecessary noise which may colour opinions early on. [↩]

One of the concepts we emphasize at Equidam is the inversion of qualitative and quantitative factors in startup valuation, as you go from Seed1 to pre-IPO funding.

The archetypal Seed startup (perhaps just an idea) has nothing to measure. Investors must use their imagination, peer into the future, project a scenario. On the other hand, a startup raising the last round of private capital before an IPO will be weighed and measured almost entirely on financial metrics.

Even as early as Series A you have access to some useful data. Can they actually build the thing? Do customers really want it? Does anyone want to work there? All sources of rich signal to help you make an objective decision about the company.

Seed is different. Success comes down to the quality and consistency of your subjective, independent judgement. In many ways it is a unique discipline within the strategy of venture.

What happens if you try to find a path in the data?

Essentially, it’s a hunt for outliers with no shortcuts and two specific qualifiers for any investment strategy:

Any attempt to pattern-match to past success is going to dramatically limit your pool of opportunity, with no clear upside.

Any constraints built into your investment strategy (sector, region, industry) are essentially a sacrifice of volatility (potential alpha).

Thus, the ideal Seed investor is likely to be a generalist, with no preconceptions about what great founders look like, where they come from, or what they might be building.

Rather than the hubris of a (supposed) rockstar stock-picker, Seed investors will find confidence through constructing solid processes, systematically rewarding good decisions and mitigating bad ones.

Finally, and perhaps most importantly, they’ll have a firm grip on the biases which manifest in all forms of investing. Particularly the curse of overconfidence which erodes the positive influence of success.

In summary, considering all of the above, we should expect Seed investors to present with an idiosyncratic worldview, some robust fundamental skills and an appetite for risk.

Sadly, reality is the opposite: Seed investors are often risk-averse herd animals with little real competence. They have Rick Rubin-esque affectations, pontificating on ‘taste’ and ‘craft’, while copying each other’s homework and hiding deep insecurity.

In the last 15 years we’ve seen the emergence of a Startup Industrial Complex, where a treadmill of capital, services and brand-strength was offered to participating firms and startups. If you wanted quick, reliable markups and easy downstream financing for your portfolio then you hopped on board.

This movement destroyed the institutional contrarianism of Seed investing. Billions of dollars were piled into safe SaaS money-printers when capital was cheap. When the market for safe investments was saturated, investors responded by dumping huge sums of capital into silly ideas (remember NFTs?).

That’s “risk”, right?

This worked during ZIRP, because everything was going up and to the right. Public markets were so cracked-out on COVID and cheap capital that they grabbed anything at IPO. But it was never going to last.

Seed VCs (and their LPs) need to recognise that role is, and always has been, to find breakout companies before they are obvious. Not to compete for deals. Not to seek validation from colleagues. To find those outliers. To be uncomfortably idiosyncratic. That’s it. That’s everything.

Critically, while it may lag by a decade or so, everything else is downstream from Seed.

The entire venture capital strategy depends on Seed investors doing their job properly. The entire premise of venture-backed innovation, and the promise of venture-scale returns, are entirely dependent on the health of Seed.

(image source: “Venice; the Grand Canal from the Palazzo Foscari to the Carità”, by Canaletto)

The story of venture capital (and its precursors) is a story of risk. You can take this back as far as you like, from ARDC to Christopher Columbus. From whaling expeditions to space exploration.

Risk is the product.

And, essentially, it boils down to this calculation:

The merit of any investment depends on whether the probability of success multiplied by the forecasted return is greater than the cost.

Investments that are perceived to have a high probability of success attract a lot of competition.

Investments that are perceived to have a low probability of success attract very little competition.

Venture capital is at the far end of this spectrum, where the ‘skill’ is in recognising when the market has mispriced risk because an idea is unconventional rather than bad.

This brings us to the first category of risk in this conversation: idiosyncratic risk.

Idiosyncratic Risk

(the specific risk of an investment)

Idiosyncratic risk reflects the specific potential of an investment: the probability of success, and the assumed return if it is succesful.

Assuming you cannot change the probability of success or the assumed return, there are two ways to handle idiosyncratic risk:

Making low probability investments profitable by diversifying away total failure.1

These are the two main levers of venture capital, which is focused on what Howard Marks refers to as uncomfortably idiosyncratic investments:

The question is, do you dare to be different? To diverge from the pack is required if you’re going to be a superior in anything. Number two, do you dare to be wrong? Number three, do you dare to look wrong? Because even things which are going to be right in the long run, maybe look wrong in the short run. So, you have to be willing to live with all those three things, different, wrong, and looking wrong, in order to be able to take the risk required and engage in the idiosyncratic behavior required for success.

Idiosyncratic risk contrasts with the other main category of risk that investors must consider: systematic risk.

Systematic Risk

(broader market-related risk)

If idiosyncratic risk is typified by venture capital, then systematic risk is typified by index funds. Consider the extent to which index fund performance is influenced by individual companies versus major political or economic events.

Nevertheless, systematic risk is a consideration in venture capital, and there are two ways to handle it:

Avoid consensus, where competition drives up prices without increasing success rate or scale.

Avoid market-based pricing, where macro factors can drive up prices without increasing success rate or scale.

Exposure to systematic risk essentially destroys an investor’s ability to properly manage (and extract value from) idiosyncratic risk.

Alpha vs Beta

If we consider idiosyncratic risk as the source of ‘alpha’ (ability to beat benchmarks) in venture capital, systematic risk reflects the ‘beta’ (convergence with benchmarks).

A striking shift in venture capital over the last 30 years, particularly the last 15, is the extent to which the balance has shifted from idiosyncratic risk to systematic risk. This is a consequence of prolonged ‘hot market’ conditions, where consensus offers a mirage of success.

Consider a typical VC in 2025. They’re likely to be focused on AI opportunities, guided by pattern-matching and market pricing (aka, “playing the game on the field”). Investing, in this scenario, is reduced to a relatively simple box-checking exercise.

All of this implies significant systematic risk; the firm is riding beta more than they are producing alpha. This creates extreme fragility.

Systematic risk has always been a concern, but it has been amplified in recent years by cheap capital and social media. The herd has grown larger and louder; more difficult for inexperienced or insecure investors to ignore:

Taking systematic risk means following the crowd. It’s an easier story to sell LPs, and there’s less career risk if it goes wrong as accountability is spread across the industry.

Taking idiosyncratic risk means wandering freely. It’s tough to spin into a coherent pitch, and there’s more obvious career risk associated with the judgement of those investments.

Despite mountains of theory and evidence supporting idiosyncratic risk as the source of outperformance, it’s just not where the incentives lie for venture capital.

The Jackpot Paradox

There are fundamental consequences of the drift towards systematic risk in venture capital:

The muscles of portfolio construction and valuation atrophy, as consensus-driven ‘access’ dominates behavior and idiosyncratic risk falls out of favour.

The typical ‘power law’ distribution of outputs collapses as few genuine outliers can be realised from a concentrated pattern of investment.

As returns converge on a mediocre market-rate, investors manufacture risk by feeding power law back into the system as an input, trying to create outlier returns.

Success is further concentrated in a system that becomes increasingly negative sum overall.

This broadly summarises where we’re at today. A disappointing scenario that represents failure to the actual bag-holders on the LP end, failure to founders, and failure to innovation.

A lot of the blame falls in the lap of LPs. The low fidelity interface with GPs means that LPs have a general bias towards compelling stories which invite systematic risk.

Thus, venture capital is reduced to a wealth-destroying competition for access to the hottest deals, fundamentally at odds with the concept of ‘uncomfortably idiosyncratic’ risk and generating alpha.

Show me the incentive and I’ll show you the outcome

Charlie Munger

One of the most thought-provoking articles in venture last year was Jamin Ball’s “Misaligned Incentives“, in which he talked about the difference between 2% firms and 20% firms.

The 2% firms are optimizing for deployment. The 20% are optimizing for large company outcomes. There’s one path where the incentives are aligned.

The article was significantly because it was represented a large allocator acknowledging the issue with incentives in private markets. Not a novel take on the problem, but resounding confirmation.

Ball stopped short of suggesting an alternative incentive structure, which was probably wise given visceral opposition to change. Many influential firms have grown fat and happy in the laissez-faire status quo of venture capital.

Ball — like many people, myself included — framed carried interest as the ‘performance pay’ component of VC compensation. The problem is implicit: we have therefore accepted that fees are not connected to performance.

For decades, we’ve accepted the wisdom that carry = performance, and fees = operational pay. Nobody thought to question that reality.

Unfortuantely, for many firms (and certainly the majority of venture capital dollars under management), carry is a mirage. It exists so investors can pretend that performance is a meaningful component of their compensation while they continue optimising for scale.

European Waterfall vs. American Waterfall

European waterfall is a whole-fund approach to carry, whereby GPs don’t receive carried interest until LPs have had 1x of the fund (plus a hurdle) returned to them. American waterfall operates on a deal-by-deal approach, with a clawback provision if the fund isn’t returned (plus a hurdle).

We know the american waterfall model (while imperfect) has historically outperformed, and yet the european waterfall has become standard. Venture capital has biased towards the ‘LP friendly’ approach to carried interest, even though it reduces their carry income, because it enables more easily scaling funds.

We find strong evidence that GP-friendly contracts are associated with better performance on both a gross- and net-of-fee basis. The public market equivalent (PME) is around 0.82 for fund-as-a-whole (LP-friendly) contracts but is over 1.24 for deal-by-deal (GP-friendly) contracts.

In summary, the problem is not that VCs have picked fees over carry as the more attractive incentive, it’s that carry has been used as a smokescreen for the exploitation of fees.

Consider these few points, from the perspective of a seed GP:

If you charge a fee to manage the fund, you should not raise a successor fund without a serious step-down in those fees. Otherwise, what are you being paid for?

You should not charge management fees on investments you’re no longer truly managing. If you have no meaningful influence over a company in your portfolio, what are you being paid to do with it?

Indeed, if you’re no longer truly managing those investments, it’s incumbent on you to sell enough of your stake to lock-in a reasonable return when the opportunity is available.

If you raise a larger subsequent fund, you should be able to explain how that strategy allows you to extract a similar level of performance from a larger pool of capital. Otherwise, how can you rationally justify a larger total fee income?

Everybody knows that markups are bullshit. If you want to raise a second fund, get at least 2x back to your LPs through secondaries first. DPI is the only proof that there’s value in your investments.

None of this should be surprising or even unintuitive, and yet…

Successor fund step-downs are remarkably uncommon.

Most US funds still do fees on total comitted capital, not even fees on invested capital, never mind fees on actively managed investments.

Few GPs have a sophisticated view on early returns, with most still focusing on MOIC rather than IRR and assuming late-stage price inflation will continue.

VCs expect founders to present a coherent pitch covering growth strategy and the implicit capital requirements. The LP-GP relationship is far cruder.

The whole venture ecosystem knows markups are barely worth the paper they are written on — and yet these incremental metrics continue to drive fundraising activity.

Over the past 15 years, LPs have become so preoccupied with getting into the hottest name-brand funds that there has been little scrutiny given to the fundamental logic of terms.

In an entirely fee-based environment, without carry as a smokescreen for bad actors, fees would likely be more clearly connected to performance — addressing the concerns laid out above.

This has the benefit of being a more predictable approach to compensation, likely attracting more responsible fiduciaries and level-headed investors. Less swinging for the fences, and more methodical investing and steady DPI.

However, it would also mean losing an important minority of brilliant investors who are genuinely motivated by carry.1

Ending the AUM game; 100% carry

In a scenario where investors only ‘eat what they kill’, performance would matter so much — across so many dimensions — that VCs would have to very quickly develop better practices on portfolio management and liquidity.

Of course, the downside is that compensation would be heavily backloaded, with no compensation for the early years of deploying capital and developing exits. A deeply unhealthy barrier to entry for emerging managers.

What’s interesting about these two edge-cases, on opposite ends of the spectrum, is that both produce the same outcome: a greater level of professionalism, with a more sophisticated view on portfolio management and liquidity than we see today.

Clearly, neither extreme is a good option and the ideal is somewhere in the middle — with both fees and carry in the mix. However, central to incentivising better outcomes is an end the fee exploitation game, with two key realisations for LPs:

Fees must be connected to performance, in that a GP should not be able to raise another fund if they have not yet demonstrated concrete performance.

The only meaningful demonstration of performance is DPI. Fortunately, as the market embraces secondaries, it’s possible to generate meaningful DPI much sooner.

Venture capital needs to evolve alongside more distant exit horizons by making better use of secondary liquidity, more cleanly dividing the market into early and late stage strategies — which can each then better play to their strengths:

We were able to take a 1x or a 2x of the entire fund off [the table] and still be very long in that company. That locks in a legacy, locks in a return, and shortens the time to payback.

For funds like [mine], selling stock of private startups to other investors will be “75% to 80% of the dollars that [limited partners] get back in the next five years.

You sell at the B, and you actually — for us, with the way our math worked — could have a north of 3x fund. But I also wouldn’t want to give up the future upside. We actually ran that through the C and the D. The big ‘Aha’ for me was that selling at the Series B, a little bit, was actually very prudent for a couple of reasons.

With all of this in mind, it no longer unreasonable for LPs expect something like a 2x return on their capital by year 6, and for VCs to raise new funds based on hitting that 2x target. Ensuring a decent return (on an IRR basis) for their LPs while companies are still within their orbit of influence.2

Unsurprisingly, proposals to fix fee income are unpopular, and not only with those who profit from the status quo. There is a lack of systems thinking which would allow participants to grasp the interconnected factors which shape outcomes, and see the opportunity for change.3

secondaries aren’t a good market ➝ because they’re only used to sell poor quality assets ➝ so they’re not a good market

returns in venture come from a few giant outcomes ➝ so we hold to IPO ➝ so more value accrues to a few survivors ➝ so most of the returns come from a few giant outcomes

you can’t get liquidity on markups➝ because they’re optimised for fees not liquidity ➝ so markups aren’t liquid

In essence, power law and illiquidity are both absolutely realities of the venture strategy, but both have also been used to excuse and entrench suboptimal practices.

The Opportunity of Secondaries

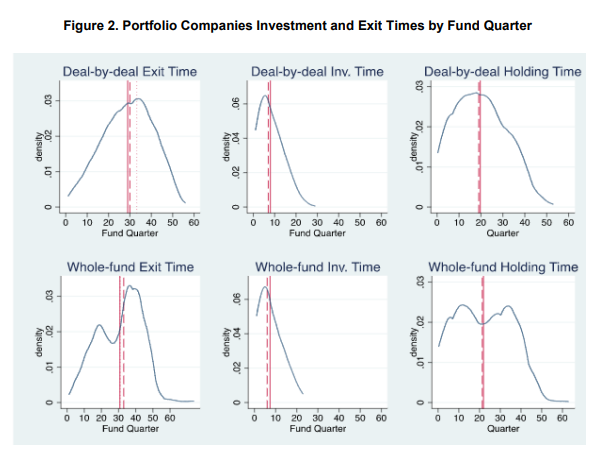

A common misconception: the value of investments increases consistently (even exponentially) over time, so GPs should always hold to maturity. This idea has played a significant part in slowing down the use of secondary transactions. It’s not really true.

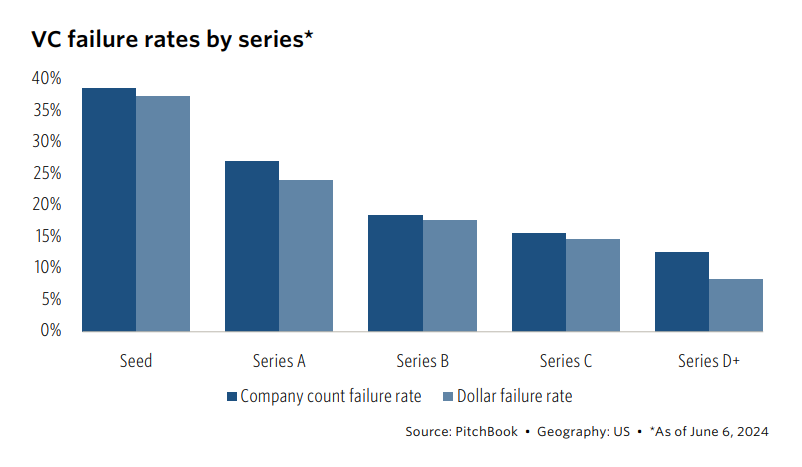

Investments often don’t increase in value. Quite often, they fail outright. Failure rate does reduce over time (39% at seed, 13% at series D), but it remains significant throughout.

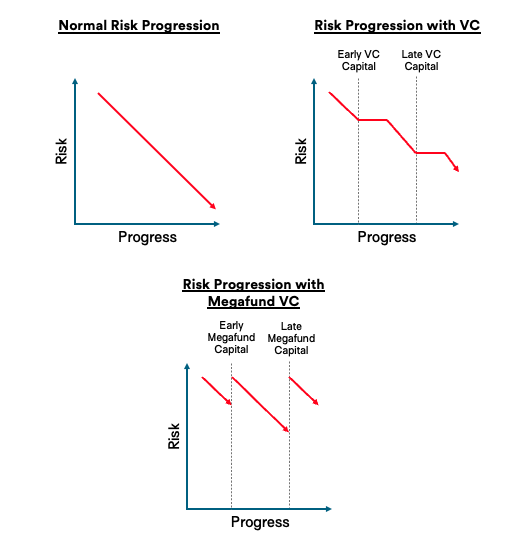

Typically, you think of a series A startup as less risky than a seed startup, and a series D startup as less risky than a series A startup. This is often true, but because VC dollars both add and remove risk, the move down the risk curve is less linear.

This is especially true for ‘the biggest winners’ who are often absorbing huge amounts of capital from the ‘venture banks’:

But in recent years, this picture has been skewed even more, especially if the capital raised comes from a mega VC fund. At each funding round, there is a significant re-risking of the startup, to the point that you are not moving meaningfully down the risk curve for a long long time. And even at a late stage, a mega funding round can bring you right back up to the point of maximum risk.

These rounds are also often highly dilutive; particularly with the proclivity of large firms to ignore pro-rata and cram-down early investors.

So, in an absolute sense, there is a sustained risk of failure which slowly concentrates portfolio returns into fewer companies over time, which will decelerate TVPI growth (or even turn it negative).

On top of that, there are often terms included in later rounds which mean that shares held by early investors become relatively overvalued. Particularly, IPO ratchet clauses and automatic conversion vetos. Thus, even if the theoretical TVPI of a seed fund remains flat, in reality it may be falling:

“In November 2015, Square went public at $9 per share with a pre-IPO value of $2.66 billion, substantially less than its $6 billion post–money valuation in October 2014. The Series E preferred shareholders were given $93 million worth of extra shares because of their IPO ratchet clause. This reinforces the idea that these shares were much more valuable than common shares and that Square was highly overvalued.”

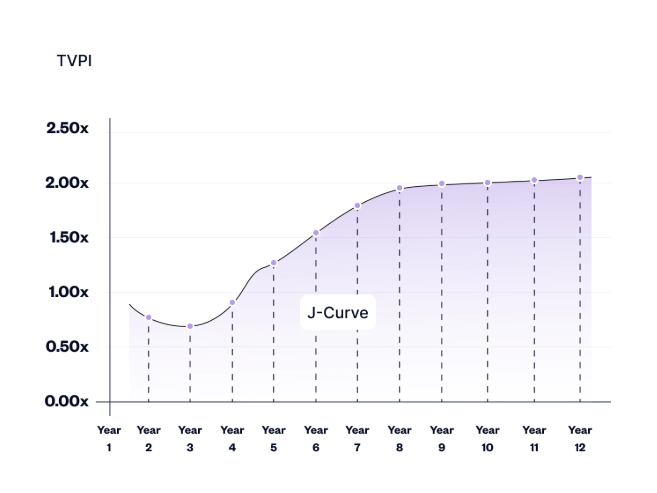

Looking at AngelList data, the best time for a fund to sell (on an IRR basis, and ignoring the clauses above) would be year 8 — with value concentrating (but not really net expanding) in years 9 through 12.

That means the typical investment (assuming a 3 year deployment period) would be best positioned for a (partial) sale in years 5-7. Considering this, it’s difficult to make the case that GPs should be holding 100% for the ultimate outcome, every time. If they do, they are concentrating their risk without necessarily improving the portfolio outcome.

To take this a step further, we could assume in a more rational market, less dominated by hype (more secondary activity driving more pricing tension, fewer bullshit markups), the illustrated TVPI would flatten out more gradually — so less of an obvious time to sell.

In short, the story here is not about opportunistic secondaries to drive better IRR. The real case to be made is for a comprehensive secondaries strategy, and opportunistic holding. For too long, there has been ideological friction around secondaries which has held back venture performance and enabled some very bad habits. It’s time to change that.

If there’s a chance to wipe the slate clean for venture capital, for LPs and GPs to return to first principles on compensation, incentives and ideal outcomes — to begin aligning venture capital with a high-performing meritocracy — it’s here, today.

Ironically, innovations in venture capital haven’t kept pace with the companies we serve. Our industry is still beholden to a rigid 10-year fund cycle pioneered in the 1970s. As chips shrank and software flew to the cloud, venture capital kept operating on the business equivalent of floppy disks. Once upon a time the 10-year fund cycle made sense. But the assumptions it’s based on no longer hold true, curtailing meaningful relationships prematurely and misaligning companies and their investment partners.