The technology industry has always celebrated scale.

From the industrial revolution to the moving assembly line, the rise of computing, and onward into the cloud. Technology and scale have become synonymous.

In many ways, that’s worth celebrating. Scale enables otherwise unworkable economics, allowing solutions that can benefit a much greater share of the population.

But this clearly doesn’t hold eveywhere, all the time.

Veblen Goods

On one end of the spectrum, there’s the iPhone. Accessible to most people in developed economies, popular amongst students, and similarly carried by all of the world’s trillionaires.

On the other end, there’s fashion. Here the world is tiered from polyester fast-fashion up to artisanal italian garms.

Fashion is a veblen good; purchasing decisions are driven by exclusivity and prestige. Whatever level of quality a scaled manufacturer may reach, they will be outdone by someone paying blind monks to weave silk from spiders in a cave.

Phones, on the other hand, all do the same thing. Even caring about owning the latest model is seen as a bit low status. Companies have tried to market luxury phones, but it never works for the simple fact that the objective specs are knowable.

The simple difference between these two worlds is mystique, or a lack of it.

Fashion sells a story. The product is how it makes you feel, not what it is. The same for wine, perfume, watches, etc.

Phones sell function. That’s it.

Confidence Men

Veblen goods cannot be scaled. In fact, these industries will often artificially constrain supply to maintain an aura of exclusivity.

Indeed, any product that can scale without appearing to lose quality is implicitly a commodity that will be evaluated on objective metrics.

Commodity products benefits from economies of scale, and costs will usually reduce as output increases. On the other hand, veblen industries occasionally raise prices to signal prestige.

There are only two exceptions to this framework. One is “elite” management consulting, and the other is “tier-1” venture capital.

They are exceptions because like a commodity what they do is fundamentally scalable, but like a veblen good it is not actually what they sell.

Elite management consultants do not sell consulting, and tier-1 venture capital firms do not sell capital. They both sell confidence to institutions, and scale helps them to create that confidence. Thus, they short-circuit the usual economic argument that veblen goods implicitly don’t scale or that commodities get cheaper at scale. They’re neither, really.

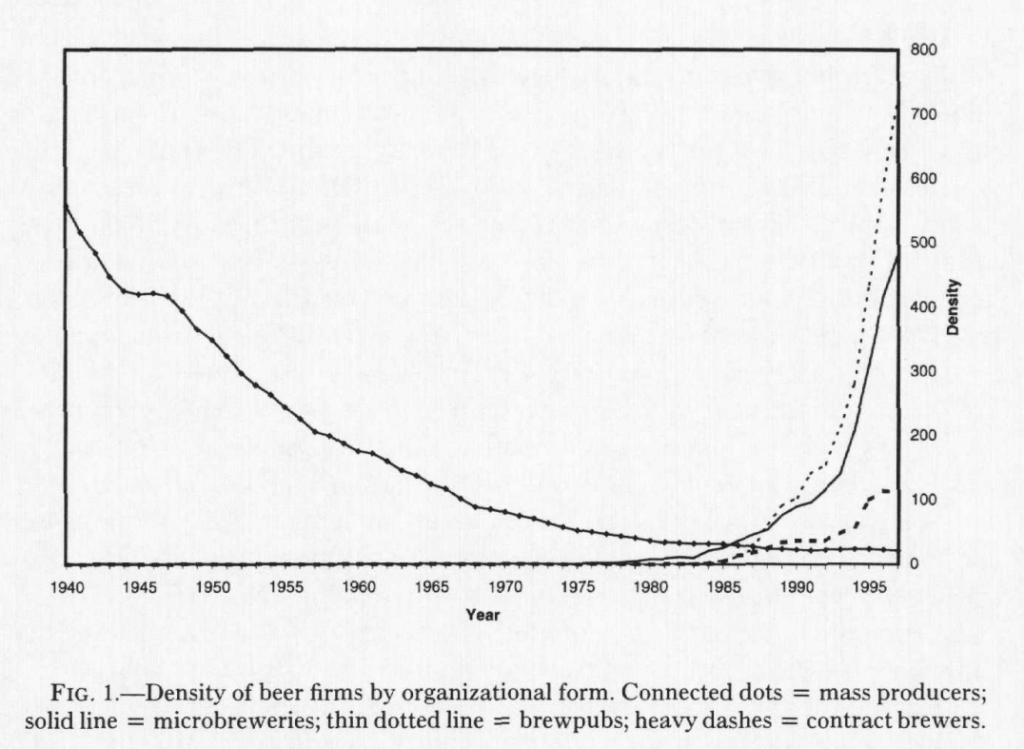

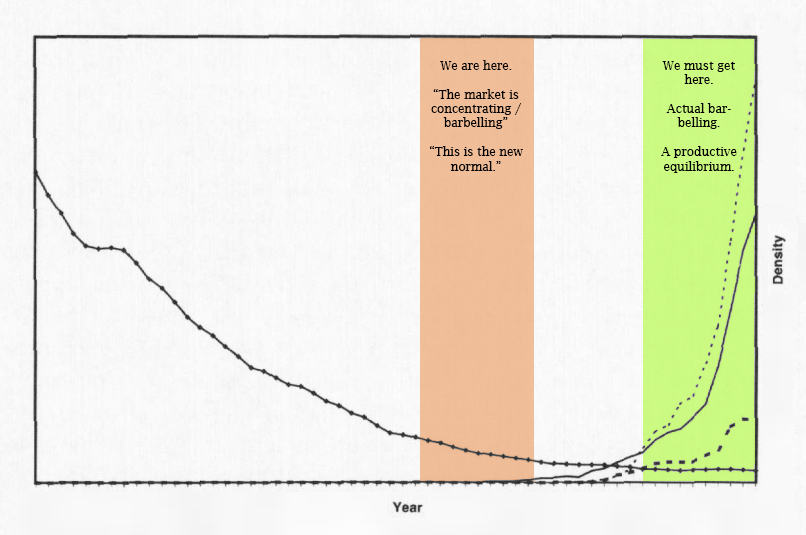

As a result, these industries are resistant to the usual economic pattern of “barbelling”; the divergence of industries into high-fee specialists and low-fee generalists. The growth of scaled venture capital and management consulting has been at the relative expense of the rest of the market.

To the extent that their proposition is to reduce organisational friction by creating confidence that drives action, there is some value being created by their service.

What remains is whether there’s actually any merit to the action itself, which is a separate but important question.

The Tilt

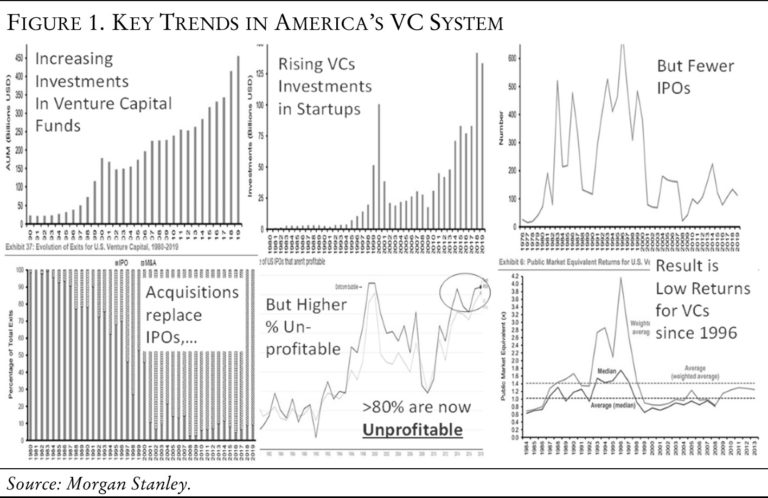

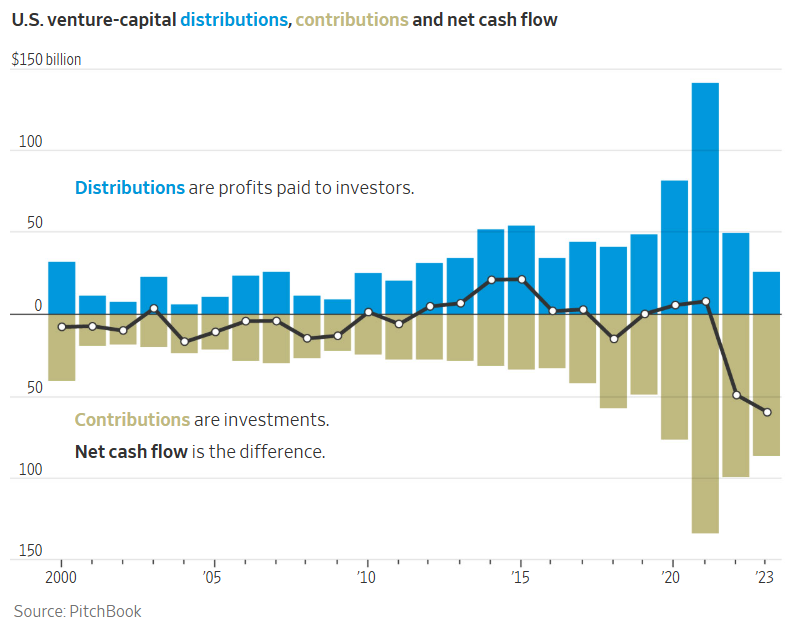

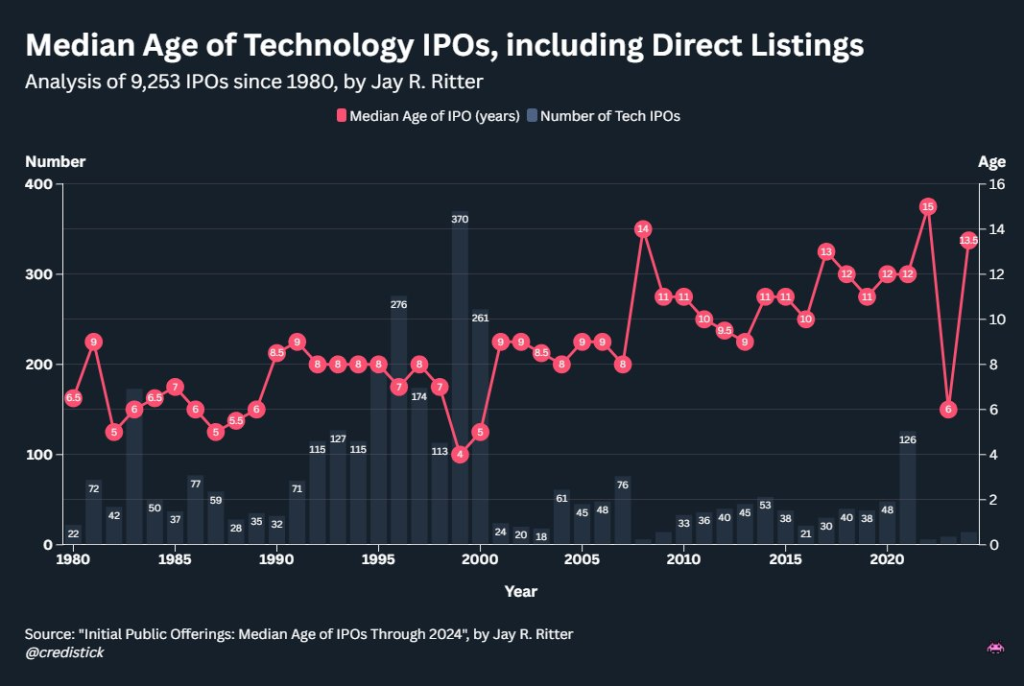

On top of this, venture capital has a bizarre structural flaw where choices and consequences are not evenly distributed. This prevents the typical corrections of a healthy market.

For the last 15 years, the largest funds have grown roughly 10x in size. As a result, they invest in larger and later rounds, so exits have been either delayed or destroyed entirely. Their large, patient LPs can tolerate this. They’re in it for stable IRR at scale to launder volatility. Exits don’t really matter.

However, the smaller and inherently more liquidity sensitive LPs that fund early-stage firms cannot. As a result of the weak liquidity environment, created by mega-funds, they have retreated from the market.

So, a snowballing percentage of the capital in each vintage goes to large funds. This has been true for the whole post-GFC period, for all that it just recently became a topic of concern.

Trend Chasers

Companies like Shein emerged on the back of social media driving frenzied buying behavior. So, while fashion is one of the archetypal veblen goods, their hack was to scale coolness with an entirely different kind of temporal signalling.

Essentially, while the goods are still the low quality output of a mass-manufactured process, they reflect something else. A particular celebrity moment, influencer promotion, or just a viral trend. It shows the world that this person is in the group.

This became possible because Shein can produce at scale on a remarkable turnaround. They use this to their advantage by providing clothes for the moment. Not only participating in the trend, but directly fuelling its inflation. Rather than taste, which is hard to scale, this requires simple opportunism, which is not.

There are parallels here to venture capital, and the ability of scaled allocators to exploit similar trends. If a category has the required elements to become hot, they can spin up a multi-billion dollar fund relatively quickly, and doing so doesn’t require any taste of their own.

This is not dissimilar to the manner in which management consultants expand and exploit movements like ESG or AI safety for incredible gain.

Things That Don’t Scale

As Shein is not inclined to come up with interesting new designs or present themselves in the market as a taste-maker, the same is true for scaled venture capital or management consultants. To make an independent judgement would be to assume risk.

Fundamentally, they exist to exploit trends where they can assign responsibility elsewhere, rather than to stand out.

However, Shein exists at the opposite end of the market to boutique fashion houses that are responsible for innovation and creating new trends that may be exploited. Meanwhile, scaled venture capital (for the reasons described above) has been busy cannibalising end of the industry.

In essence, venture capital has sacrificed intellectual diversity and creativity in the pursuit of just mindlessly managing more capital. As a result, the industry is quite visibly worse at recognising and funding the kind of outliers that create important innovation.

In fact, if you take Elon Musk out of the equation (and so no SpaceX, Tesla or OpenAI) it’s really questionable how much progress we’d have seen in the last 25 years.

What’s troubling about all this is that there is no obvious cyclical correction. The free market is not coming to save anyone.

{kind=link}