Private markets have inherited the curse of myopia

It’s a long held belief that public markets may be a poor environment for innovation because of the short-term focus driven by meeting quarterly targets.

However, there’s an indication that this has reversed.

Research from the 1990s and early 2000s did indicate that public companies invested less, and were less responsive to investment opportunities than matched private peers, as a reflection of limited long-term thinking in their strategy.

“Listed firms invest less and are less responsive to changes in investment opportunities compared to observably similar, matched private firms, especially in industries in which stock prices are particularly sensitive to current earnings.”

Comparing the Investment Behavior of Public and Private Firms, by John Asker, Joan Farre-Mensa and Alexander Ljungqvist

However, this does not appear to be the case in more recent analysis. In a relative sense, comparing public companies to matched private companies, public companies now appear to be more long-term oriented than their private peers.

“IPO firms respond more to investment opportunities and have higher productivity in their early public years. Our results on public firms’ sensitivity to growth opportunities hold under several robustness tests, including when we consider firms’ total growth including acquisitions.”

Do IPO Firms Become Myopic?, by Vojislav Maksimovic, Gordon Phillips and Liu Yang

What has changed over the course of the last 25 years which could explain this? Primarily, the volume of capital in private markets, and the scale of exits.

Venture capital has evolved from the business of funding cheap / high ROI experiments to the business of fuelling market expansion. As a result, it has inherited what was once a public market problem; the need to regularly demonstrate growth in order to boost share price.

Today, revenue targets for the various staged funding rounds are surging, as expectations climb higher and creep earlier.

In the late 2010s it was assumed that a company could comfortably hit a Series A with around $1M in revenue. That rose to $2-3M by 2024, and with AI the bar has been pushed even further in the years since.

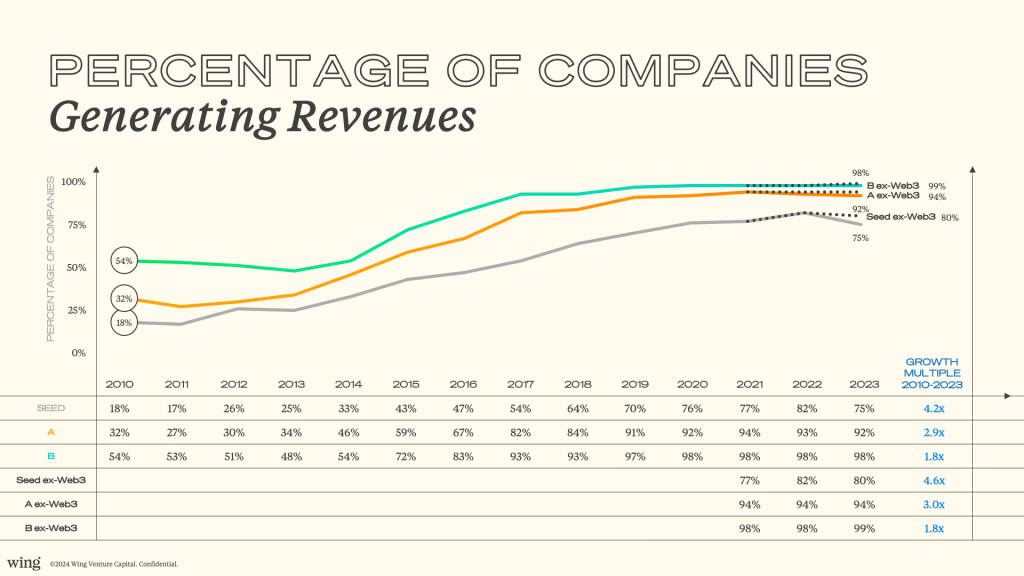

Consider data from Wing. Only 32% of Series A companies had any revenue at all in 2010, growing to 92% by 2023.

More than ever, venture capitalists want to see revenue. And once you have revenue, it will never be enough.

The resulting myopia problem is a real problem for innovation, and there’s both a robust empirical case and a important anecdotal case to be made.

The Academic Case

First up, the data. There’s a strong case made across a number of papers about the dangers of startups scaling too soon, and too quickly.

“We find that startups that begin scaling within the first 12 months of their founding are 20–40% more likely to fail… [We also find] no evidence of a countervailing benefit in terms of successful exit.”

When Do Startups Scale? Large-scale Evidence from Job Postings, by Saerom (Ronnie) Lee and J. Daniel Kim

“For the last 6 months the Startup Genome Project has been researching what makes high growth technology startups successful and has gathered data on more than 3200 startups. In our research one reason for failure has shown up again and again: premature scaling.”

Startup Genome Report Extra on Premature Scaling, Max Marmer, Bjoern Lasse Herrmann, Ertan Dogrultan and Ron Berman

To provide a summary of the obvious, it is crucial that startups scale properly across all dimensions as they develop. They must be testing and validating assumptions, adding the right skills at the right time, and building the right core of knowledge.

If you want long-term compounding growth from a genuinely important company, it probably doesn’t start with a mad dash to build a flimsy book of contracted ARR.

When startups are pushed — by the incentives presented by investors — to pursue “growth at all costs”, this obviously produces much more brittle businesses. As a result, they fail more often, innovate less, have higher rates of fraud, and produce worse exits.

The Anecdotal Case

It’s an interesting thought-experiment to apply this question of short-termism and long-termism to the world of AI.

On one hand, there is Google, a public company. Fundamentally, today’s AI industry would not exist without Google, DeepMind, and their pioneering work on the transformer architecture.

While they’ve been slower to commercialise the technology than some of their private peers, they have caught up quickly and regularly trade the top-spot on benchmarks with the other labs.

Perhaps, more importantly, is the calm demeanour and steady leadership reflected by Demis Hassabis. He talks about science, curing disease, and other productive applications of the technology with giddy optimism.

There’s a particularly powerful scene in the Thinking Game documentary where Demis comes to the conclusion that they should predict every protein sequence in existence and release the data for free to spur further discoveries.

On the other hand, there is the temperamental nature of leadership at the private labs. Altman and Amodei have spent years making reckless claims about AGI, the end of employment and parallels to weapons of mass destruction.1

This is not intended to downplay the impact of these models. There are real concerns about changes to the job market, and to cybersecurity. But for a technology is so consequential, who would you prefer as a steward? Sam “Code Red” Altman, Dario “Oppenheimer” Amodei, or Demis Hassabis?

The truth is that Altman and Amodei are bound by the need to play the private market game. If either one of them falls significantly behind on revenue growth, investors will herd toward their competitor. So, they are stuck in an incremental battle for market share and short-term narrative victories. They are slaves to the needs of their investors, inflating the impact of their work beyond all reason.

Meanwhile, Hassabis is quietly building. He does not need to go on speaking tours, drum-up investor interest or pump the market with irrational sentiment. He’s responsible (along with the other great researchers across Google) for far more important innovation than the other private labs combined.

In this example, it is clearly the public market tortoise that is beating the private market hare in the long-run.

Private Market Myopia

The tragedy of a more myopic private market is that even as it grows in scale and scope, it is not able to fund the innovations which have been crying out for more patient capital.

Instead of driving capital into long-horizon infrastructure and industrial capacity, swollen private markets pursue endless incrementalism — an acusation they have commonly levelled at the public markets.

Worse still, is this myopia feeds investment in short-term opportunities that cannibalise long-term prosperity. Predatory lending companies, “pay-to-earn” scams, expense gambling apps and crypto casinos. These well-funded corners of the market are not only an opportunity cost for real innovation, but are actively cannibalising future potential.

So, yes. The world will need more great public companies to help dig us out of this casino economy.

- Occasionally with times and locations that coincided with major private market fundraising activity. [↩]

Leave a Reply