There’s a weird phenomenon among VCs where the less successful they are, the more evil they become to founders to squeeze more money out of their best startups out of necessity which then becomes a vicious cycle of adverse selection.

Garry Tan, President & CEO of Y Combinator

Including the above, criticism of venture capital often applies a fairly broad-brush, which might feel unfair.

If you look a little closer, you’ll see it’s actually a problem of venture capital’s own making. An identity has emerged over the last decade which feels like an attempt to homogenise the asset class. This has been characterised by gatekeeping, consensus seeking, exclusionary behaviour, protectionism of networks and relationships, determining the ‘in-group’ and then restricting access to it.1

This identity appears at the core of venture capital, thanks to the gravitational effect of extreme insecurity: with so little in the way of transparent standards, particularly on measuring performance, most managers look for implicit validation from their peer group. They adopt the same attitude, use the same jargon, invest in the same categories, and follow the same practices.2

Toxicity seems to be compensation for insecurity in our industry. It’s not good.

Eric Bahn, Co-Founder & GP at Hustle Fund

Unfortunately, that group is clearly a negative force, having a chokehold on the public image of the asset class and an unfortunate influence on the overall returns.

Adverse Selection

If you follow finance and economics, you will be familiar with the problem of adverse selection. For those that aren’t, here a rough summary of the explanation from Nobel winning economist, George Akerlof, and his famous paper, “The market for lemons”:

Buyers in the used car market aren’t typically mechanics, so struggle to judge whether their potential purchase is in good shape or a bucket of rust with a new paint-job.

This imbalance of information between buyers and sellers creates a reluctance to ever pay full price – until eventually everyone selling good cars is driven out of the market.

To apply this to venture capital: you have a category of managers who deal with their performance anxiety by blending into the herd – aiming for consensus, not excellence. The ones who smirk when managers set ambitious targets, despite that being the name of the game.

These managers are the buyers in this analogy, hedging their bets out of uncertainty in their own ability, benchmarking against averages, and ultimately degrading the whole asset class.

Feedback Loops

I’ve written at length about why standards for measuring performance in VC are important, and how that could be addressed. But why does it matter, and what do we mean when we refer to insecurity amongst managers?

For this, there’s no better analogy than The Monkey Problem, which I believe is credited to Astro Teller, Captain of Moonshots at X:3

Imagine you tell 100 people that their goal is to have a monkey on a pedestal reciting Shakespeare, 100 days from now. They know that you might check up on them along the way, and are concerned about demonstrating their progress.

The first thing everyone is going to spend time on is finding or making the most impressive pedestal, because that is the most attainable and demonstrable sign of progress – even if it is trivial compared to teaching the monkey.

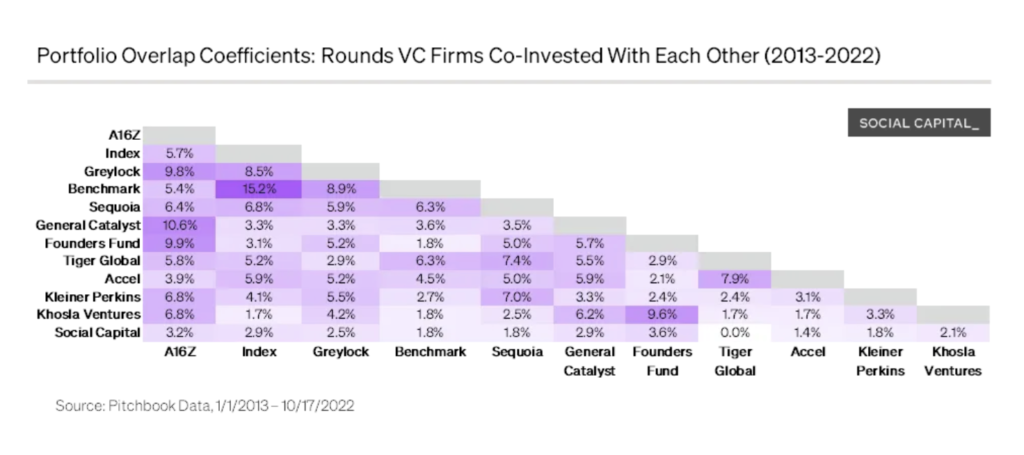

In venture capital, the pedestal equivalent is the logo hunting, where managers will seek to invest in hot deals, or invest alongside ‘tier 1’ firms, in order to have those logos on their LP updates. It’s a superficial sign of “progress”, and has no direct relation to the real goal of generating returns. They don’t really know how well they are performing on those terms, and they can’t really compare themselves to their peers.4

Turns out, when you’re building a venture firm truly from scratch (limited track record, no Ivy, didn’t work in venture prior, etc.), logos + investing alongside name brands matter far more than anything else.

Eric Tarczynski, Founder and Managing Partner at Contrary

Monkeys and Lemons

To join the two together: the monkey problem creates the information asymmetry (inability to understand fund performance) which results in the lemon problem (the drift towards measuring manager performance via relationships and how well they fit the stereotype).

As a result, there’s increasing gravity around that ‘in-group’ network of VCs, and fitting into those patterns of behaviour and identity. It’s that group which becomes the subject of so much (often deserved) criticism, and the target of parody.

Managers who do not identify with this group are de facto not the target of that criticism. They are secure enough in their ability to not need to adopt the superficial signals of competence. Through their implicit understanding that venture capital is precisely not about fitting a pattern, they are likely to outperform those that follow the herd. Unfortunately they often face an up-hill struggle when raising successive funds.

This has a deeply concerning impact on the performance of venture capital, and the quality of ventures they back, as well as the diversity of founders and ideas that will be funded.

VCs may subconsciously be looking for founders who share similarities with themselves and may not be able to effectively assess founders who have exceptional but different qualities.

Nnamdi Okike and Aaron Holiday, of 645 Ventures

The solution to this, going back to the root of this problem, is to focus on the monkey.

Every stakeholder in the process, from founders to LPs, need to be clear that their responsibility is generating returns. There needs to be a real shift towards making and measuring returns, rather than assigning value to relationships and hype.

Specifically, for an informative approach with practical feedback windows (quarterly or annual, rather than decennial), that requires making TVPI a meaningful metric through standardised methodologies and transparent reporting.

This is never going to happen without some kind of broad industry consensus, which in turn is unlikely to happen while the ‘in-group’ VCs dominate the narrative and control what success looks like to protect their own necks.

For those who are holding on to the belief that venture capitalists are the last bastion of smart money, it is time to let go. While there are a few exceptions, venture capitalists for the most part are traders on steroids, riding the momentum train, and being ridden over by it, when it turns.

Professor Aswath Damodaran, Wall Street’s “Dean of Valuation”

(top image: Pieter Bruegel the Elder’s “The Parable of the Blind Leading the Blind”)

- Not to mention the patagonia vest, vacations in Mykonos, or how many times they can squeeze ‘grok’ or ‘rubric’ into a conversation. [↩]

- Once-upon-a-time it was popularly characterised by ‘VC Twitter’, though that weird ecosystem has become more self-aware and at least partially a self-parody. [↩]

- The moonshot factory, not the social media platform [↩]

- We also discussed this during a recent episode of the Equidam podcast. [↩]