The story of venture capital (and its precursors) is a story of risk. You can take this back as far as you like, from ARDC to Christopher Columbus. From whaling expeditions to space exploration.

Risk is the product.

And, essentially, it boils down to this calculation:

The merit of any investment depends on whether the probability of success multiplied by the forecasted return is greater than the cost.

Investments that are perceived to have a high probability of success attract a lot of competition.

Investments that are perceived to have a low probability of success attract very little competition.

Venture capital is at the far end of this spectrum, where the ‘skill’ is in recognising when the market has mispriced risk because an idea is unconventional rather than bad.

This brings us to the first category of risk in this conversation: idiosyncratic risk.

Idiosyncratic Risk

(the specific risk of an investment)

Idiosyncratic risk reflects the specific potential of an investment: the probability of success, and the assumed return if it is succesful.

Assuming you cannot change the probability of success or the assumed return, there are two ways to handle idiosyncratic risk:

Making low probability investments profitable by diversifying away total failure.1

These are the two main levers of venture capital, which is focused on what Howard Marks refers to as uncomfortably idiosyncratic investments:

The question is, do you dare to be different? To diverge from the pack is required if you’re going to be a superior in anything. Number two, do you dare to be wrong? Number three, do you dare to look wrong? Because even things which are going to be right in the long run, maybe look wrong in the short run. So, you have to be willing to live with all those three things, different, wrong, and looking wrong, in order to be able to take the risk required and engage in the idiosyncratic behavior required for success.

Idiosyncratic risk contrasts with the other main category of risk that investors must consider: systematic risk.

Systematic Risk

(broader market-related risk)

If idiosyncratic risk is typified by venture capital, then systematic risk is typified by index funds. Consider the extent to which index fund performance is influenced by individual companies versus major political or economic events.

Nevertheless, systematic risk is a consideration in venture capital, and there are two ways to handle it:

Avoid consensus, where competition drives up prices without increasing success rate or scale.

Avoid market-based pricing, where macro factors can drive up prices without increasing success rate or scale.

Exposure to systematic risk essentially destroys an investor’s ability to properly manage (and extract value from) idiosyncratic risk.

Alpha vs Beta

If we consider idiosyncratic risk as the source of ‘alpha’ (ability to beat benchmarks) in venture capital, systematic risk reflects the ‘beta’ (convergence with benchmarks).

A striking shift in venture capital over the last 30 years, particularly the last 15, is the extent to which the balance has shifted from idiosyncratic risk to systematic risk. This is a consequence of prolonged ‘hot market’ conditions, where consensus offers a mirage of success.

Consider a typical VC in 2025. They’re likely to be focused on AI opportunities, guided by pattern-matching and market pricing (aka, “playing the game on the field”). Investing, in this scenario, is reduced to a relatively simple box-checking exercise.

All of this implies significant systematic risk; the firm is riding beta more than they are producing alpha. This creates extreme fragility.

Systematic risk has always been a concern, but it has been amplified in recent years by cheap capital and social media. The herd has grown larger and louder; more difficult for inexperienced or insecure investors to ignore:

Taking systematic risk means following the crowd. It’s an easier story to sell LPs, and there’s less career risk if it goes wrong as accountability is spread across the industry.

Taking idiosyncratic risk means wandering freely. It’s tough to spin into a coherent pitch, and there’s more obvious career risk associated with the judgement of those investments.

Despite mountains of theory and evidence supporting idiosyncratic risk as the source of outperformance, it’s just not where the incentives lie for venture capital.

The Jackpot Paradox

There are fundamental consequences of the drift towards systematic risk in venture capital:

The muscles of portfolio construction and valuation atrophy, as consensus-driven ‘access’ dominates behavior and idiosyncratic risk falls out of favour.

The typical ‘power law’ distribution of outputs collapses as few genuine outliers can be realised from a concentrated pattern of investment.

As returns converge on a mediocre market-rate, investors manufacture risk by feeding power law back into the system as an input, trying to create outlier returns.

Success is further concentrated in a system that becomes increasingly negative sum overall.

This broadly summarises where we’re at today. A disappointing scenario that represents failure to the actual bag-holders on the LP end, failure to founders, and failure to innovation.

A lot of the blame falls in the lap of LPs. The low fidelity interface with GPs means that LPs have a general bias towards compelling stories which invite systematic risk.

Thus, venture capital is reduced to a wealth-destroying competition for access to the hottest deals, fundamentally at odds with the concept of ‘uncomfortably idiosyncratic’ risk and generating alpha.

Show me the incentive and I’ll show you the outcome

Charlie Munger

One of the most thought-provoking articles in venture last year was Jamin Ball’s “Misaligned Incentives“, in which he talked about the difference between 2% firms and 20% firms.

The 2% firms are optimizing for deployment. The 20% are optimizing for large company outcomes. There’s one path where the incentives are aligned.

The article was significantly because it was represented a large allocator acknowledging the issue with incentives in private markets. Not a novel take on the problem, but resounding confirmation.

Ball stopped short of suggesting an alternative incentive structure, which was probably wise given visceral opposition to change. Many influential firms have grown fat and happy in the laissez-faire status quo of venture capital.

Ball — like many people, myself included — framed carried interest as the ‘performance pay’ component of VC compensation. The problem is implicit: we have therefore accepted that fees are not connected to performance.

For decades, we’ve accepted the wisdom that carry = performance, and fees = operational pay. Nobody thought to question that reality.

Unfortuantely, for many firms (and certainly the majority of venture capital dollars under management), carry is a mirage. It exists so investors can pretend that performance is a meaningful component of their compensation while they continue optimising for scale.

European Waterfall vs. American Waterfall

European waterfall is a whole-fund approach to carry, whereby GPs don’t receive carried interest until LPs have had 1x of the fund (plus a hurdle) returned to them. American waterfall operates on a deal-by-deal approach, with a clawback provision if the fund isn’t returned (plus a hurdle).

We know the american waterfall model (while imperfect) has historically outperformed, and yet the european waterfall has become standard. Venture capital has biased towards the ‘LP friendly’ approach to carried interest, even though it reduces their carry income, because it enables more easily scaling funds.

We find strong evidence that GP-friendly contracts are associated with better performance on both a gross- and net-of-fee basis. The public market equivalent (PME) is around 0.82 for fund-as-a-whole (LP-friendly) contracts but is over 1.24 for deal-by-deal (GP-friendly) contracts.

In summary, the problem is not that VCs have picked fees over carry as the more attractive incentive, it’s that carry has been used as a smokescreen for the exploitation of fees.

Consider these few points, from the perspective of a seed GP:

If you charge a fee to manage the fund, you should not raise a successor fund without a serious step-down in those fees. Otherwise, what are you being paid for?

You should not charge management fees on investments you’re no longer truly managing. If you have no meaningful influence over a company in your portfolio, what are you being paid to do with it?

Indeed, if you’re no longer truly managing those investments, it’s incumbent on you to sell enough of your stake to lock-in a reasonable return when the opportunity is available.

If you raise a larger subsequent fund, you should be able to explain how that strategy allows you to extract a similar level of performance from a larger pool of capital. Otherwise, how can you rationally justify a larger total fee income?

Everybody knows that markups are bullshit. If you want to raise a second fund, get at least 2x back to your LPs through secondaries first. DPI is the only proof that there’s value in your investments.

None of this should be surprising or even unintuitive, and yet…

Successor fund step-downs are remarkably uncommon.

Most US funds still do fees on total comitted capital, not even fees on invested capital, never mind fees on actively managed investments.

Few GPs have a sophisticated view on early returns, with most still focusing on MOIC rather than IRR and assuming late-stage price inflation will continue.

VCs expect founders to present a coherent pitch covering growth strategy and the implicit capital requirements. The LP-GP relationship is far cruder.

The whole venture ecosystem knows markups are barely worth the paper they are written on — and yet these incremental metrics continue to drive fundraising activity.

Over the past 15 years, LPs have become so preoccupied with getting into the hottest name-brand funds that there has been little scrutiny given to the fundamental logic of terms.

In an entirely fee-based environment, without carry as a smokescreen for bad actors, fees would likely be more clearly connected to performance — addressing the concerns laid out above.

This has the benefit of being a more predictable approach to compensation, likely attracting more responsible fiduciaries and level-headed investors. Less swinging for the fences, and more methodical investing and steady DPI.

However, it would also mean losing an important minority of brilliant investors who are genuinely motivated by carry.1

Ending the AUM game; 100% carry

In a scenario where investors only ‘eat what they kill’, performance would matter so much — across so many dimensions — that VCs would have to very quickly develop better practices on portfolio management and liquidity.

Of course, the downside is that compensation would be heavily backloaded, with no compensation for the early years of deploying capital and developing exits. A deeply unhealthy barrier to entry for emerging managers.

What’s interesting about these two edge-cases, on opposite ends of the spectrum, is that both produce the same outcome: a greater level of professionalism, with a more sophisticated view on portfolio management and liquidity than we see today.

Clearly, neither extreme is a good option and the ideal is somewhere in the middle — with both fees and carry in the mix. However, central to incentivising better outcomes is an end the fee exploitation game, with two key realisations for LPs:

Fees must be connected to performance, in that a GP should not be able to raise another fund if they have not yet demonstrated concrete performance.

The only meaningful demonstration of performance is DPI. Fortunately, as the market embraces secondaries, it’s possible to generate meaningful DPI much sooner.

Venture capital needs to evolve alongside more distant exit horizons by making better use of secondary liquidity, more cleanly dividing the market into early and late stage strategies — which can each then better play to their strengths:

We were able to take a 1x or a 2x of the entire fund off [the table] and still be very long in that company. That locks in a legacy, locks in a return, and shortens the time to payback.

For funds like [mine], selling stock of private startups to other investors will be “75% to 80% of the dollars that [limited partners] get back in the next five years.

You sell at the B, and you actually — for us, with the way our math worked — could have a north of 3x fund. But I also wouldn’t want to give up the future upside. We actually ran that through the C and the D. The big ‘Aha’ for me was that selling at the Series B, a little bit, was actually very prudent for a couple of reasons.

With all of this in mind, it no longer unreasonable for LPs expect something like a 2x return on their capital by year 6, and for VCs to raise new funds based on hitting that 2x target. Ensuring a decent return (on an IRR basis) for their LPs while companies are still within their orbit of influence.2

Unsurprisingly, proposals to fix fee income are unpopular, and not only with those who profit from the status quo. There is a lack of systems thinking which would allow participants to grasp the interconnected factors which shape outcomes, and see the opportunity for change.3

secondaries aren’t a good market ➝ because they’re only used to sell poor quality assets ➝ so they’re not a good market

returns in venture come from a few giant outcomes ➝ so we hold to IPO ➝ so more value accrues to a few survivors ➝ so most of the returns come from a few giant outcomes

you can’t get liquidity on markups➝ because they’re optimised for fees not liquidity ➝ so markups aren’t liquid

In essence, power law and illiquidity are both absolutely realities of the venture strategy, but both have also been used to excuse and entrench suboptimal practices.

The Opportunity of Secondaries

A common misconception: the value of investments increases consistently (even exponentially) over time, so GPs should always hold to maturity. This idea has played a significant part in slowing down the use of secondary transactions. It’s not really true.

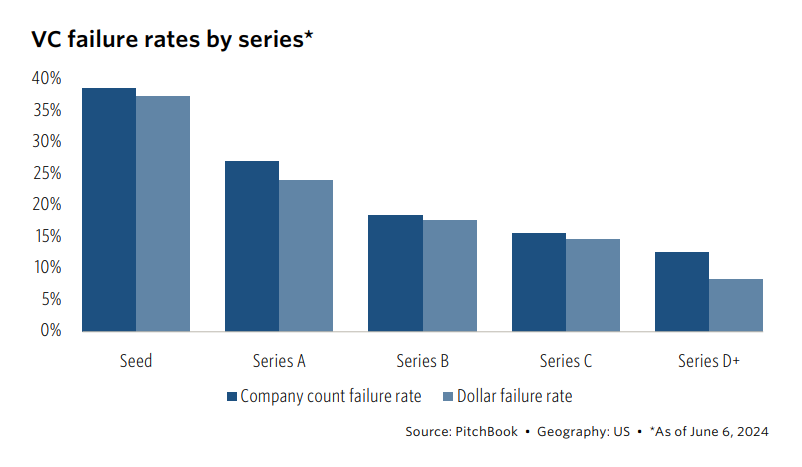

Investments often don’t increase in value. Quite often, they fail outright. Failure rate does reduce over time (39% at seed, 13% at series D), but it remains significant throughout.

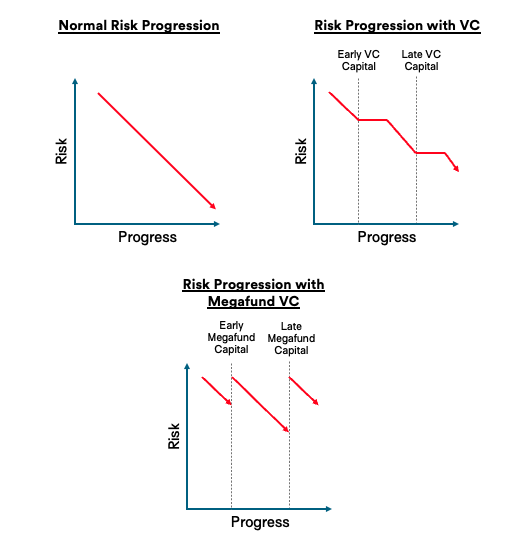

Typically, you think of a series A startup as less risky than a seed startup, and a series D startup as less risky than a series A startup. This is often true, but because VC dollars both add and remove risk, the move down the risk curve is less linear.

This is especially true for ‘the biggest winners’ who are often absorbing huge amounts of capital from the ‘venture banks’:

But in recent years, this picture has been skewed even more, especially if the capital raised comes from a mega VC fund. At each funding round, there is a significant re-risking of the startup, to the point that you are not moving meaningfully down the risk curve for a long long time. And even at a late stage, a mega funding round can bring you right back up to the point of maximum risk.

These rounds are also often highly dilutive; particularly with the proclivity of large firms to ignore pro-rata and cram-down early investors.

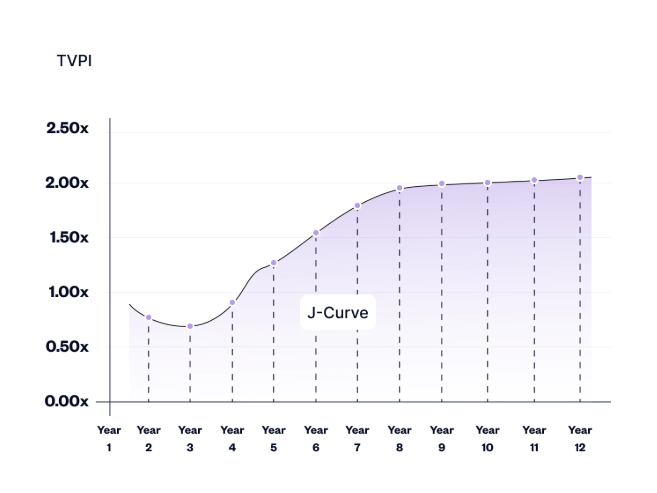

So, in an absolute sense, there is a sustained risk of failure which slowly concentrates portfolio returns into fewer companies over time, which will decelerate TVPI growth (or even turn it negative).

On top of that, there are often terms included in later rounds which mean that shares held by early investors become relatively overvalued. Particularly, IPO ratchet clauses and automatic conversion vetos. Thus, even if the theoretical TVPI of a seed fund remains flat, in reality it may be falling:

“In November 2015, Square went public at $9 per share with a pre-IPO value of $2.66 billion, substantially less than its $6 billion post–money valuation in October 2014. The Series E preferred shareholders were given $93 million worth of extra shares because of their IPO ratchet clause. This reinforces the idea that these shares were much more valuable than common shares and that Square was highly overvalued.”

Looking at AngelList data, the best time for a fund to sell (on an IRR basis, and ignoring the clauses above) would be year 8 — with value concentrating (but not really net expanding) in years 9 through 12.

That means the typical investment (assuming a 3 year deployment period) would be best positioned for a (partial) sale in years 5-7. Considering this, it’s difficult to make the case that GPs should be holding 100% for the ultimate outcome, every time. If they do, they are concentrating their risk without necessarily improving the portfolio outcome.

To take this a step further, we could assume in a more rational market, less dominated by hype (more secondary activity driving more pricing tension, fewer bullshit markups), the illustrated TVPI would flatten out more gradually — so less of an obvious time to sell.

In short, the story here is not about opportunistic secondaries to drive better IRR. The real case to be made is for a comprehensive secondaries strategy, and opportunistic holding. For too long, there has been ideological friction around secondaries which has held back venture performance and enabled some very bad habits. It’s time to change that.

If there’s a chance to wipe the slate clean for venture capital, for LPs and GPs to return to first principles on compensation, incentives and ideal outcomes — to begin aligning venture capital with a high-performing meritocracy — it’s here, today.

Ironically, innovations in venture capital haven’t kept pace with the companies we serve. Our industry is still beholden to a rigid 10-year fund cycle pioneered in the 1970s. As chips shrank and software flew to the cloud, venture capital kept operating on the business equivalent of floppy disks. Once upon a time the 10-year fund cycle made sense. But the assumptions it’s based on no longer hold true, curtailing meaningful relationships prematurely and misaligning companies and their investment partners.

While GenAI can improve worker efficiency, it can inhibit critical engagement with work and can potentially lead to long-term overreliance on the tool and diminished skill for independent problem-solving. Higher confidence in GenAI’s ability to perform a task is related to less critical thinking effort.

In colder markets, founders just need capital on reasonable terms, and it doesn’t really matter where it comes from. Value-add propositions and brand strength are less important; access to hot companies doesn’t move the needle as much for LPs. Instead they care more about differentiation through strategy.

In hotter markets, the opposite is true. Investors will be chasing the fastest growing companies in the most attractive categories, out on the thin ice of excess risk. LPs, sold the same dream, care only about how GPs can parlay their way into those deals. How you invest is irrelevant, what matters is your network and your brand.

Strangely, at the peak things begin to come full circle. In 2021, when there the incredible amount of capital was spread across a record 1,594 firms, there was a horseshoe effect: with such abundant opportunity for investment, LPs and VCs once again saw the opportunity in strategy-driven alpha.

In normal circumstances, the next stage of this cycle is the crash. The firms that leaned the hardest into chasing heat would be the most exposed, with portfolios that are the most obviously out of alignment with value. What’s left are the firms who chose to focus on solid strategy, who can begin harvesting deals in the down market.

In 2022, this shift was derailed by the emergence of venture banks, designed to escape the typical cycles of venture. The largest firms raised the most capital in subsequent years. Access remained an important part of the story for LPs, especially with the convenient rise of AI.

In fact, you could argue that this was the second time that cycle was disrupted, as many experienced investors called the top in 2016-2018 only to be thwarted by COVID. Two years of intense, irrational enthusiasm for digital only exacerbated the problem.

The Importance of Cycles

Consider how much of the natural world has evolved alongside fire. Wildfires serve an important purpose in preventing ecosystems from choking themselves to death on redundant biomass, and there are even species that have evolved to use fire as a mechanism to spread their seeds.

Humanities view of fire as a threat, and the goal of suppressing it entirely in the natural environment, has had disastrous consequences. We have seen the emergence of ‘mega-fires‘, where biomass accumulates to the point where spread is fierce and inevitable.

There’s a compelling parallel to venture capital. The extent to which the market is suffering today is proportional to the amount of time it took to hit a correction. There’s even a ‘redundant biomass’ problem of zombie unicorns.

What’s worse, for reasons described above we haven’t yet really allowed the full cycle to complete.

Forcing a Reset

While venture banks steam off into the distance, and venture capital tries to figure out how to navigate this environment, there are three signs of change.

Increasingly, there’s talk of smaller LPs like family offices looking to pursue direct investing strategies. In theory, this affords them a similar level of risk with better economics, but questions remain about their bandwidth to do this properly.

There’s been a surprising number of high profile GP departures, both launching their own funds and not. In many cases, this means partners are giving up wharever carry incentive they had. This suggests some discomfort in the status quo.

An increasing number of founders talking about bootstrapping or ‘seedstrapping’ (one and done fundrasing), or other strategies to avoid the problems assocaited with getting on the venture capital treadmill and the expectations involved.

For the GPs that remain, it’s time to consider what the world would look like if the cycle had completed. How would they be forced to act in a truly ‘down market’ environment. Indeed, if you consider that many smaller firms have been priced out of AI, that may already feel like their reallity.

It is clear that the bar for performance is significantly higher in a cash constrained environment with higher interest rates. While that may not change the reality for venture banks, it is existential for traditional venture capital.

The ‘Knowledge Work’ Problem

In hot markets, where investors take a prescriptive approach to investment, there is a huge problem with atrophy. Completely separate to the poor investments that come out of these periods, it’s also worth examining the practices they establish.

Investors that spend all of their time chasing hot deals based on a number of set criteria have the same basic problem as knowledge workers that rely on Generative AI solutions: they are not using their critical thinking muscles. Executing orders, not problem solving.

Consider how little actual thinking you have to do about an investment if your process is focused on second-order factors. Is it on an a16z market map, is it on YC’s Request for Startups, are other “tier 1” investors are in the round? Will downstream investors will give you the markups you need, and will LPs will be excited about it?

This behavior, geared towards capital velocity, is focused on second order information and pattern matching. It is a prescriptive approach that informs what gets investment, displacing the first-order considerations about things like team, opportunity, valuation, market and strategy.

This dissertation focuses exclusively on moral hazard, which refers to a venture capitalist’s propensity to exert less effort and shirk their fiduciary duties to the investors to maximize their self-interest; specifically, a VC’s propensity to choose subjective selection criteria over more cognitively taxing objective criteria when faced with multiple options and fewer resource restrictions.

While this approach might broadly work for venture banks, with an army of low-impact investors looking to index across new technology trends, it will not deliver the returns required by the traditional venture model.

This might sound like cowboy investing. A Rick Rubin-esque vibes based approach to venture capital. It certainly can be, and if you happen to be Rick Rubin it might just work — but why take the risk?

The way for these investors to operate from a position of strength is to build process alpha. That is, do everything you can to prevent being wrong for predictable reasons (controlling for bias), and to manage the risk of being completely wrong a lot of the time (portfolio construction). Not to overintellectualise investment decisions, but to give yourself the strongest foundation to embrace the risk of uncertainty.

To take the analogy a bit further, for all that Rick Rubin is a total eccentric, guided by his own taste without the need for external validation, he is not cavalier about it. He pays immense attention to environment and routine in order to help him get the best return on his time.

There’s never a need for investors to stray from this disciplined mode of operation, it just so happens that most are prey to the cycles of venture capital and the temptation to inflate fees when opportunity arises.

Discpline is easy when opportunity is limited. (top image: “Lesnoi pozhar (Forest Fire)”, by Aleksej Kuzmich Denisov-Uralsky)

In venture capital circles, the most widely discussed trend of 2024 (outside of AI) has been the concentration of capital into “venture banks” like Andreessen Horowitz, General Catalyst and Thrive Capital. The household names of venture capital have had a blockbuster year, while others carefully ration the tail-end of their last fund.

The first quarter opened with Andreessen Horowitz and General Catalyst scooping up 44% of the available capital. 2024 is closing on a similar note, with 9 firms having captured more than half of all funds raised so far. The 30 most capitalized firms this year collectively represent three quarters of the pool raised by at least 380 funds.

However, the real anomaly is not how much the large funds have raised, but rather how poorly everyone else has done. Why has the bottom fallen out of the market for smaller funds, if the giant firms are still able to vacuum up capital?

Ask a hundred GPs or LPs where they draw the line between small funds and large funds, or how they define multi-stage and multi-sector strategies, and you will get a hundred different answers. The lack of standard definitions and common understandings has dramatically hindered productive discourse about venture capital over the years.

Importantly, it has obscured the manner in which multi-stage venture capital has diverged from the rest of the market. Today, it operates a novel model for startup investment, targeting a new class of LPs with a very different premise.

A Rapacious Playbook

In 2011, Jay Levy of Zelkova Ventures wrote an article about the conflicting interests involved in insider pricing. His point was simple: when investors led rounds for existing portfolio companies, their desire for greater ownership would be outweighed by their need to show performance.

Two things are striking about this article:

Jay’s concern probably seems alien or overly-dramatic to anyone who entered venture capital within the last decade. Today, it’s just the game on the table.

It is also likely to be the single largest contributing factor to the pricing bubble that grew during ZIRP and exploded in 2022, if you follow the incentives created.

In a rational market, where VCs are all stage-specific, each round of investment has a different lead investor. That means, at regular intervals in the company’s development, it will be valued by a neutral third-party. Outside investors that want to maximize ownership will go up against founders that want to limit dilution. From that tension, we expect a generally fair outcome to emerge.

Venture capital relies on this tension, and the increasing financial savvy of investors as the investment moves downstream, stewarding companies toward exits. From qualitative analysis at the earliest stages to the quality of cash flow at maturity; you move the dial from founder strength to financial performance as you go from pre-seed to IPO, and so the expertise of investors evolves in parallel.

Multi-stage firms have a different (and fairly rapacious) view on this process. Instead of inviting scrutiny of the value of their portfolio companies, their strategy is to keep that in-house, or within a network of associated firms. Rather than rational pricing through the tension of buyer and seller, they have embraced the jagged edge of what Jay Levy described: why worry about valuation if pricing can be a competitive advantage?

Want 3-4x markups on investments to show LPs? Just do subsequent rounds at 3-4x and get them rubber-stamped by networked investors. With “performance” taken care of, it’s easier to raise more capital to feed portfolio companies, fuelling aggressive growth to grow into those markups. It’s putting the cart before the horse, compared to conventional venture thinking, but it has a certain brutal charm.

So, we’re beginning to see that the ‘capital as a competitive advantage’ playbook didn’t expire with ZIRP. A decade of cheap capital was what it took to prove the model, and today it just needs a different class of LP to back it. Indeed, multi-stage GPs appear to have spent 2023 with their heads down, consolidating around the best-looking secondary opportunities (SpaceX, OpenAI, Anthropic, Anduril) ahead of a grand tour in the Middle East. Sovereign wealth, with giant pools of capital and no great pressure on liquidity, are complementary to the traditional large institutional LPs for this strategy.

Exploiting Venture Capital’s Flaws

As multi-stage firms have expanded their funds under management, they’ve had to similarly scale their ability to capture market share. This has been solved through a fairly innovative list of features, each of which exploits a different dynamic of venture markets:

Platform Teams: Leaning into size as an advantage, multi-stage VCs have built platform teams with the advertised intent to offer support and resources to portfolio companies. In reality, portfolio teams are the serfs of the venture world, managing the burden of a large portfolio for a relatively small team of partners while generally adding little value for founders.

Signalling Risk: VCs are wildly vulnerable to herd behavior. An example of this is “signalling risk”: concern about the signal of how other investors respond to a startup. Despite being obviously silly, this essentially means “tier 1” firms get prima nocta on every founder they touch, so they scoop them up en masse with scout programs and EIR initiatives.

Backing GPs: While the rest of the market struggles, multi-stage funds can raise additional vehicles through which they become LPs in emerging managers. They look like the good guys, supporting the underdogs, broadening the market and encouraging competition. In fact, they are entrenching centralized positions in the relationship model of venture capital.

Operator Investors: In the last decade, there has been an ideological shift towards the idea of ‘operator investors’. Former founders are seen as the ideal archetype for venture capital, having first-hand experience building companies. As it turns out, they don’t really make for better investors, they’re just extremely well networked and have credibility with founders.

Procyclical Pricing: A huge amount of valuation wisdom has been discarded over the last decade, as the industry as a whole adapted to deal velocity with cruder pricing models—e.g. revenue multiples, raise/ownership, etc. These common practices lack critical specificity and amplify volatility in the market, a problem for venture firms that rely on rational pricing.

The Value of Venture Beta

The product of this multi-stage approach to startup investment is “venture beta”: returns will broadly track the market, while they expand in network, assets, and market share. For the largest institutional LPs, like sovereign wealth, this is fine: acceptable returns with minimal volatility, and they can brag about funding innovation with the support of the most prestigious firms.

Further out, this model’s success depends on whether it can produce companies that are attractive to public market investors or private market acquirers. Up to now, large infusions of capital with crude pricing have produced sloppy, undisciplined businesses. The IPO market is still reeling from being force-fed companies with poor financial health in 2021. Whether this misalignment can be fixed, or is inherent to the strategy, has yet to be seen.

Some early stage VCs have commented that multi-stage VCs still rely on small, contrarian firms to identify opportunities before they are ‘legible’. It seems more accurate to say that small firms are just another source of signal about new market opportunities for the mutli-stage strategy, rather than a crucial part of the chain. Scout programs, hackathons and accelerators all create redundancy for the competence of small firms in this capacity.

For Those Seeking Alpha

While historical patterns would indicate that the funding will bounce back for everyone else next year, it is worth some urgent reflection on how the growing share of multi-stage capital influences the market.

In the short term, multi-stage firms tapping into a new LP base shouldn’t have a huge impact on smaller funds, although many of their usual LPs will be spooked by the shift. GPs should have a good answer for how they adapt to this reality. How can they compete against the capital, network and brand strength of multi-stage firms in future? With increasing skepticism about the “value add” from venture capitalists, what do they offer founders that the multi-stage firms can’t?

For GPs with high domain expertise in hard sciences, there is enough evidence of outperformance to differentiate them from large generalists. For everyone else, the burden of proof is going to be higher than ever, and will require becoming disciples of venture theory: Read everything there is about portfolio construction, historical performance, decision making, biases and strategy, and build a rock-solid case for LPs that you deliver on the two critical fronts:

The potential to deliver excellent returns, in contrast to the mediocre performance of the largest firms. Not by swinging for the fences on every hit, but with properly optimized portfolio, price discipline, and solid understanding of the underlying theory.

Backing the best founders with the most important ideas. However good a multi-stage fund gets at identifying early stage opportunities, their model will always bias towards consensus themes and capital-intensive ideas. It is a limitation.

Essentially, GPs of smaller funds need to meet divergence with divergence, and embrace the strengths of their size and strategy: contrarianism and discipline, which amount to a form of value investing for early stage companies. Finding the easily overlooked. The alpha.

The Fork in the Road

Multi-stage GPs spent the last decade cosplaying as VCs, despite their practices being opposed to the conventional rationale of venture capital. You can’t make good judgements about price vs value or question consensus themes if your existence is predicated on assigning arbitrary markups and chasing the hottest companies.

Over the last decade, many VCs have sought to emulate “tier 1” multi-stage behavior, acting out what they believe LPs and peers expect to see despite the fundamentally incompatible models. This herding around identity and behavior reflects the extreme level of insecurity in venture capital, a product of the long feedback cycles and futility of trying to reproduce success in a world of exceptions. It has also produced some extremely poor practices, and bad attitudes.

The more VCs study the history, theory and current reality of private market activity, the more conviction they can develop about their own mindset as investors. The more confidence they have, the better they will fare as individuals in a discipline where peer-validation is poison and the herd is always wrong.

If that’s not for you, then there is a lucrative future to be had working at a venture bank.

The venture capital industry, once lauded for its role in fostering innovation and technological breakthroughs, has lost its way. The pursuit of hyperscalable software companies, fueled by incentives tied to management fees and opaque valuation practices, has led VCs to prioritize short-term gains over long-term value creation.

This shift has effectively sidelined deep tech startups in favor of software ventures that, while initially promising high margins, often end up as structurally unsustainable and unattractive in the eyes of public markets and acquirers.

The liquidity crisis and the collapse of valuations post-2022 are, to a large extent, the result of this myopic focus.

Markups, Management Fees, and Misaligned Incentives

The core problem lies in how venture capital funds are structured. Many VCs earn their income primarily through management fees, which are a percentage of the assets under management (AUM). In this framework, VCs are incentivized to raise as much capital as possible and deploy it rapidly, not necessarily into companies with the strongest long-term potential, but into those that will generate high markups quickly. The logic is simple: markups create the illusion of success, which can then be showcased to Limited Partners (LPs) as evidence of strong fund performance, enabling VCs to raise subsequent funds and further increase their management fees.

However, the criteria for these markups are alarmingly arbitrary. Without standardized metrics for valuing private companies or clear data collection methods, VCs have significant leeway to set valuations that align with their own interests. The result is an ecosystem that disproportionately rewards companies that raise as much capital as possible, at the highest valuation they can achieve, regardless of their underlying business fundamentals.

This creates a vicious cycle where capital-intensive, rapidly scaling software startups are favored over deep tech ventures. The latter, which often require years of research and development before reaching commercial viability, do not fit neatly into this model. They lack the frequent fundraising rounds that VCs rely on for quick markups and cannot be easily measured using ARR multiples which have become the venture capital industry’s (moronic) North Star.

A Crisis of Venture Capital’s Own Making

The 2022 downturn in venture-backed company valuations, especially in the SaaS sector, was a long time coming. For years, VCs funneled billions into software companies with the promise of high margins, rapid user growth, and scalable business models. But as these companies matured, the flaws in this strategy became apparent. Many of these SaaS businesses, initially rewarded for their revenue growth, began to reveal cracks in their unit economics and competitive moats.

In the public markets, where profitability, defensibility, and cash flow become the ultimate measures of value, these companies failed to meet expectations. The high-growth software playbook that worked so well in the private markets could not withstand the scrutiny of IPOs or M&A, leading to today’s slowdown in both exits and later stage valuations.

The outcome? VCs are now sitting on portfolios filled with overvalued, underperforming software companies. The lack of attractive exit opportunities has created a liquidity crisis, trapping capital in companies that may never deliver the returns expected.

The Opportunity Cost

Amidst this frenzy for rapid scaling and quick markups, deep tech has been left behind. Yet, ironically, it is these deep tech companies—whether in biotech, space tech, or hardware—that have the potential to deliver outsized returns and societal impact. Unlike SaaS companies that can be replicated with relative ease, deep tech ventures are built on defensible intellectual property, technological breakthroughs, and years of research. Their competitive moats, while difficult to establish, are significantly harder to erode.

Deep tech is fundamentally misaligned with the current VC incentive structure.1 These startups will take much longer to mature. They may not need to raise subsequent rounds until they have proven their solution, which may mean lengthy R&D cycles without easily measurable increase in value. This means fewer markups, less frequent fundraising, and, consequently, less “performance” to show to LPs.

The paradox is that while deep tech may not deliver immediate returns, its potential for outsized impact—both in terms of financial returns and societal benefits—is far greater than the current crop of SaaS investments. If successful, deep tech companies can redefine industries, create entirely new markets, and generate returns that are an order of magnitude higher than those seen in the overfunded software space.

The Return to Venture Capital’s Roots

The original mission of venture capital was to take on the risk of funding transformative technologies that traditional finance would not touch. Semiconductors, biotech, and early internet technologies were all enabled by patient capital willing to bet on the future. However, over the past decade, this ethos has been replaced by a focus on capital velocity, management fees, and the illusion of quick wins.

The solution to the current crisis is not simply more capital or better timing. It requires a fundamental realignment of venture capital with its original purpose. This means rethinking how funds are structured, how incentives are aligned, and how performance is measured. VCs need to shift away from the obsession with ARR multiples and markups toward a focus on genuine value creation, technological defensibility, and long-term impact.

In essence, the liquidity crunch facing the VC industry today is self-inflicted. By prioritizing short-term returns over sustainable value, VCs have created portfolios filled with fragile businesses ill-equipped for the demands of public markets. A return to deep tech, with its focus on defensible, transformative technologies, offers a path forward—not just for the VC industry but for the broader economy.

The future of venture capital should not be in chasing the next SaaS unicorn but in rediscovering the roots that built the industry: funding the innovations that will shape the next century. The hard pivot toward deep tech is not just a strategic necessity—it is a return to the true purpose of venture capital.

While there are welcome signs of a hard tech rennaisance in places like El Segundo, it remains an uphill battle and is largely misaligned with venture capital incentives. Indeed, the fact that companies like SpaceX and Anduril had to be started by billionaires is evidence of venture capital’s failure. [↩]

VCs taking public money (pensions, sovereigns, etc) must publicly disclose all deals, terms, marks and position changes.

LPs managing public money must publicly disclose all fund positions and cash returns.

Tax treatment for anything up to ~series A should be extremely advantageous to small managers.

No passing public money through multiple layers (e.g. VCs acting as LPs to EMs).

LPs managing public money should not offer bonuses to their allocators based on short-term performance.

LPs managing public money should have something similar to polical rules around disclosing gifts, travel, hospitality, etc.

This is just a start. The highest level changes that should be made to correct some of the perverse incentives in venture capital today, providing adequate accountability for public capital.

Venture capital is a seriously long-term game, with investments taking somewhere between 8 and 16 years to return liquidity.

The distance to that horizon creates a lot of eccentricity.

For example, VC does not reward following patterns or navigating market movements, neither of which is relevant to decade-long cycles. Consensus of pretty much any kind is toxic, as the more people agree with something the less profitable it becomes. Investment experience is like comfortable entropy, slowly eating-away at your ability to remain objective.

In a sense, success itself is antimemetic: the better the outcome of an investment, the more likely you are to try and repeat it through pattern matching — destroying the calibration which allowed you to find it in the first place.

Can you imagine how maddening that is?

This is why the best GPs are oddballs. They live with the paradox that being a ‘good investor’ is a process of constant discovery, and the more lost you feel the better you are probably doing.

It takes a certain madness to do well, and that is not something you can pick up on the job. You cannot be taught how to think in a contrarian manner. Nobody can give you the confidence required to wait a decade to see if you have good judgement. You have it, or you don’t.

This is why great VCs earn a lot of respect. The role they play in financing entrepreneurial dreams is critical. From the semiconductor origins of Silicon Valley to SpaceX and our future on other planets, someone had to be there to write the check.

If the incentives were well aligned, that’s where this story would end — as a fan-letter to weirdos. VC would remain a cottage industry investing in wacky stuff, offering strong returns for LPs.

Unfortunately, that is not the case.

Over the past decade we’ve seen the emergence of a new type of VC: one who moves between trends with the swagger of a heat-seeking missile, investing as if their money might go bad. This behavior is contrary to pretty much everything that we know about venture capital, and yet the trend has only accelerated.

To understand why, we have to look at VC compensation:

The ‘2 and 20’ structure of VC compensation is pretty well understood and has remained unchanged for a long time: You get 2% of the fund per year in ‘management fees’ to pay your bills and support portfolio companies, and 20% of ‘carried interest’ as a share in any profits made.1

For people passionate about the outliers, carried interest is the hook. Secure enough big wins and you can make a vast amount of money, in contrast to management fees which aren’t exactly lucrative for a small fund. It’s also nice that carried interest aligns success of the firm with success of the founders.

However, as capital flooded into private markets over the last couple of decades, and exits took longer to materialise, some cunning individuals recognised an opportunity: the 2% is guaranteed, independent of performance, and it is possible to ‘hack’ venture to maximise that income.

You can do things the old fashioned way, raising (for example) two $100,000,000 funds in a ten year period, with the implied annual income of $4,000,000. Alternatively, you can squeeze three funds into that period, at double the size, and scale your income to a mighty $12,000,000. All without really needing to worry about underlying performance.

To build that second scenario, you need to do three things:

Invest in the most overheated, capital-intensive industries, which allow you to justify raising and deploying larger funds ever more quickly. These industries are also an easy-sell for LPs, who want something to talk about at dinner parties.

Systematically undermine the understanding of valuation by promoting crude and illogical practices, and calling people nerds if they say things like “free cash flow”. Venture is a craft, not a science — which basically gives you carte blanche, right?

Pour capital into brand and status building for your firm, which LPs love. Celebrities, political figures, impressive offices, big events… Anything that shows them you’re a serious institution (with the perks that entails) and not some garage-band firm.

Instead of looking 8 to 16 years in the future with your portfolio, you want to focus on the next 2 to 3 years in order to align with your fundraising cycles. You want companies that are likely to grow in value rapidly in the near future, so hype and consensus are powerful allies.

The aim is to invest in a company at Seed and propel it to a Series A within 2 years at a 4-5x markup, which — if you can repeat it often enough — will look great to LPs. If they ask about DPI just talk about how the IPO markets should open next quarter next year.2

You want to make sure the heat persists, to ensure prices at later stages remain frothy and your markups get better and better. So consider a bit of thought leadership to keep interest on your chosen sector. As long as LPs believe the hype, and keep investing in other funds on that theme, capital will keep piling in. Amplify that market momentum as much as possible. Volatility is your friend, and over time it can even help you wash out smaller managers that offer an unfavourable comparison on performance.

Obviously the actual investment returns from this strategy are likely to be terrible, unless you’ve somehow timed another ZIRP/2021 exit phenomenon and can unload all of your crap on the public markets just before the music stops. It doesn’t really matter, because the median return in VC is so poor that you might just luck your way into top quartile anyway. Keep the paper marks strong, keep bullshitting LPs about the market conditions and the insane potential of whatever it is you are investing in, and you can probably keep buying back in with a new fund.

It’s going to be toxic to founders, as they watch huge piles of capital being incinerated chasing hype instead of genuine innovation.

It’s going to be toxic to VCs, as good practices around markups, pricing and portfolio management are ditched in favour of capital velocity and short-term incentives. It’s already frighteningly clear how much basic investing knowledge washed out of VC during ZIRP.

The management fee is often frontloaded and scales back after the investment period. The 20% carried interest may also have a hurdle rate (e.g. 8%) which guarantees some return on investment for LPs before they split profits with the VC. [↩]

It might not matter though, as many institutional LP allocators collect their bonuses on markups, so their incentives are totally aligned with yours. They’ll probably have moved on to a new job in a few years anyway. [↩]

In a strange twist for an asset class built on patient capital and outsized returns, finding liquidity for investors has become a matter of urgency for VCs.

On the surface, this is a story about venture capital’s evolution and fund managers adopting more sophisticated liquidity strategies. Pry a little deeper, and you’ll find LPs reneging on capital commitments, pushing VCs to secondary markets and expressing disappointment with activity over the last few years. Now, some just want to cash out.

The cash-rich environment allowed companies to grow into loftier valuations with relatively little scrutiny, while benefiting from the scrutiny of their public peers. For many this seemed like a winning strategy, with projected outcomes that were often jaw-dropping, and some VCs began talking about 15 year liquidity horizons. Significantly, there was no outcry from LPs; distant horizons were the name of the game, and the theoretical scale of returns bought a lot of patience.

Large private firms are thriving in part by freeriding on public company information and stock prices. Such firms’ astonishing ability to attract cheap capital may last only so long as public companies continue to yield vast, high-quality information covering a broad range of companies.

So why the sudden pivot to seeking liquidity in the last two years? Why are investors now so concentrated on returning capital? Is there more to this story than interest rates?

Overheating the market

The basic proposition of venture capital is that LPs commit a certain amount of capital to a VC fund and are returned some multiple of that over the following decade.

There are two unique considerations for potential investors in venture capital:

This combination makes it challenging to identify promising VC funds; track record is unreliable and performance is opaque. What remains for LPs is networks and trust, explaining why so much focus is put on relationships. These relationships, and over a decade of ultra-low interest rates, have allowed VCs to get away with longer periods of illiquidity and slipping rates of return.

Track records for evaluating VC's are an overused crutch.

LPs are programmed to use past track record as the primary driver in making a decision on whether to invest in a new fund (A recent study showed historical persistence of VC is that 70% chance a fund performs above…

The assurance offered, in place of returns, centred on the mounting theoretical value of venture portfolios. Venture-backed companies were raising vast sums from investors who thought of valuation as an ‘arbitrary milestone’ in the process. As long as the number kept going up with each new round, the investment looked good. This approach allowed VCs to raise ever-larger funds, extract more in fees, deploy more capital to inflate valuations further… and the wheel kept turning.

In theory, LPs were set for historic returns, as soon as those companies hit an exit.

The venture funding freeze

How many poorly-performing tech IPOs does it take to put public market interest on ice? In 2022, we found out.

While some point the finger at interest rates for spooking investors towards the end of 2021, the evidence of a correction was there from earlier in the year as many high-profile tech IPOs saw a rapid collapse in share price. There was a clear disconnect between tech valuations and a public market which no longer had faith in what they were being presented.

This was the consequence of venture capital’s exuberance. Shifting the focus to crude measures of current value had corrupted pricing discipline to the extent that exits were no longer viable. Any path to liquidity required coming to terms with huge markdowns, backtracking on the promised returns and damaging the trust of LPs.

To say that, in hindsight, it would have been a good idea to sell more stock in 2021 is to ignore the underlying irrationality. Had VCs been inclined to sell, valuations wouldn’t have been so high to begin with.

It was not that the strategy was bad, it was that there wasn’t one.

The path ahead for venture capital

VCs created this liquidity squeeze by exploiting an opaque market and increasingly divorcing price from value. This is precisely what needs to change in order to foster a healthy secondary market: greater transparency, discipline on valuation.

Specifically, a secondary market will only work if it is perceived to be where VCs sell their winners at a reasonable price, to account for shifts in risk profile outside of their portfolio focus. In this scenario, the incentives are built on transparency. Conversely, if the perception is that secondaries are for firms to offload companies that investors have lost faith in, then the incentives are built on obscuring or misrepresenting performance. That asymmetry leads to adverse selection and the slow death of any market it touches.

The future of venture capital has to involve greater transparency and stronger standards, to rebuild relationships with LPs, enhance market efficiency and access to liquidity. That vision requires the careful consideration of incentives, built on a fair and rational approach to understanding the value of venture investments. It means eliminating trust from the equation.

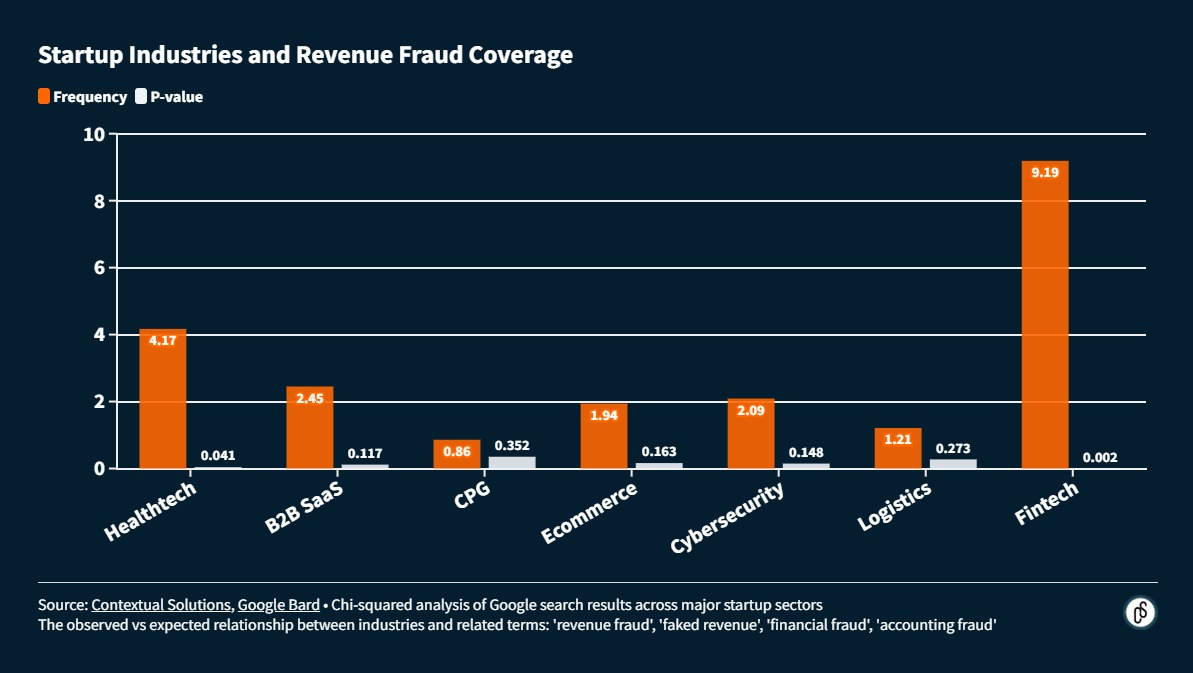

For as long as there has been business, there has been fraud, and ‘cooking the books’ is about as old as it gets. In recent years, the extreme focus on revenue has produced dangerous incentives for founders and investors to cut corners. Those chickens are now coming home to roost.

Now a regular feature in tech media, we’ve seen a growing number of cases in which startups have been caught fabricating revenue (and associated metrics like accounts, deposits, transactions, etc). Given the focus on financial performance for venture backed businesses, it has left the impression that you might escape scrutiny if your numbers look good at a glance.

The most recent examples include Banking as a Service (BaaS) up-and-comer, Solid; financial aid startup, Frank; notorious cryptocurrency exchange, FTX; and mobile money interoperability provider, Dash. It’s not deliberate that all of these examples are Fintech companies, though it does appear that Fintech is the sector most commonly associated with revenue fraud.

Is this a consequence of the fundraising environment? Is there a deeper problem in Fintech?

The pressure of hypergrowth

While venture capital has taken a much more moderate tone towards growth in 2023, with mentions of ‘quality revenue’ and ‘sustainability’, this wasn’t always the case. Up until early 2022 the strategy du jour was raising huge amounts of capital at inflated valuations in order to fund aggressive growth to try and justify said valuations.

Companies are taking on huge burn rates to justify spending the capital they are raising in these enormous financings, putting their long-term viability in jeopardy. Late-stage investors, desperately afraid of missing out on acquiring shareholding positions in possible “unicorn” companies, have essentially abandoned their traditional risk analysis.”

Nowhere has this been felt more keenly than in the Fintech industry, a darling of the venture capital industry since the post-financial crisis wave of evolution kicked off around 2010.

The startup-led digitalisation of financial products, including the ability to scale at a rate far surpassing incumbents by using a different playbook (see how Revolut has scaled internationally by adhering to just the regulatory minimums), has driven incredible revenue growth for Fintech in recent years.

After achieving more than 500% growth in 2021, the juggernaut Fintech growth finally began to stall in November. We can speculate on the reasons, but the chief suspects are the impact of COVID’s Omicron variant on business confidence, the beginning of the current surge in inflation, as well as growing fears of deeper economic woes spurred by the pandemic.

None of those factors will be much comfort to founders who will continue to try and live up to the expectations of the extreme growth demonstrated in 2021. For many investors, the benchmark has been set and the goal is to return to it, for the sake of their fund performance.

Smoke and mirrors

Even at the best of times you will see a range of behaviours, from subtle manipulation to outright fraud, in startup financials. With so much on the line, and relatively little accountability, there’s a clear incentive to cut corners.

Remember FTX was a $32bn company with no board, no accountant, no HR & no detailed due diligence prior to investment.

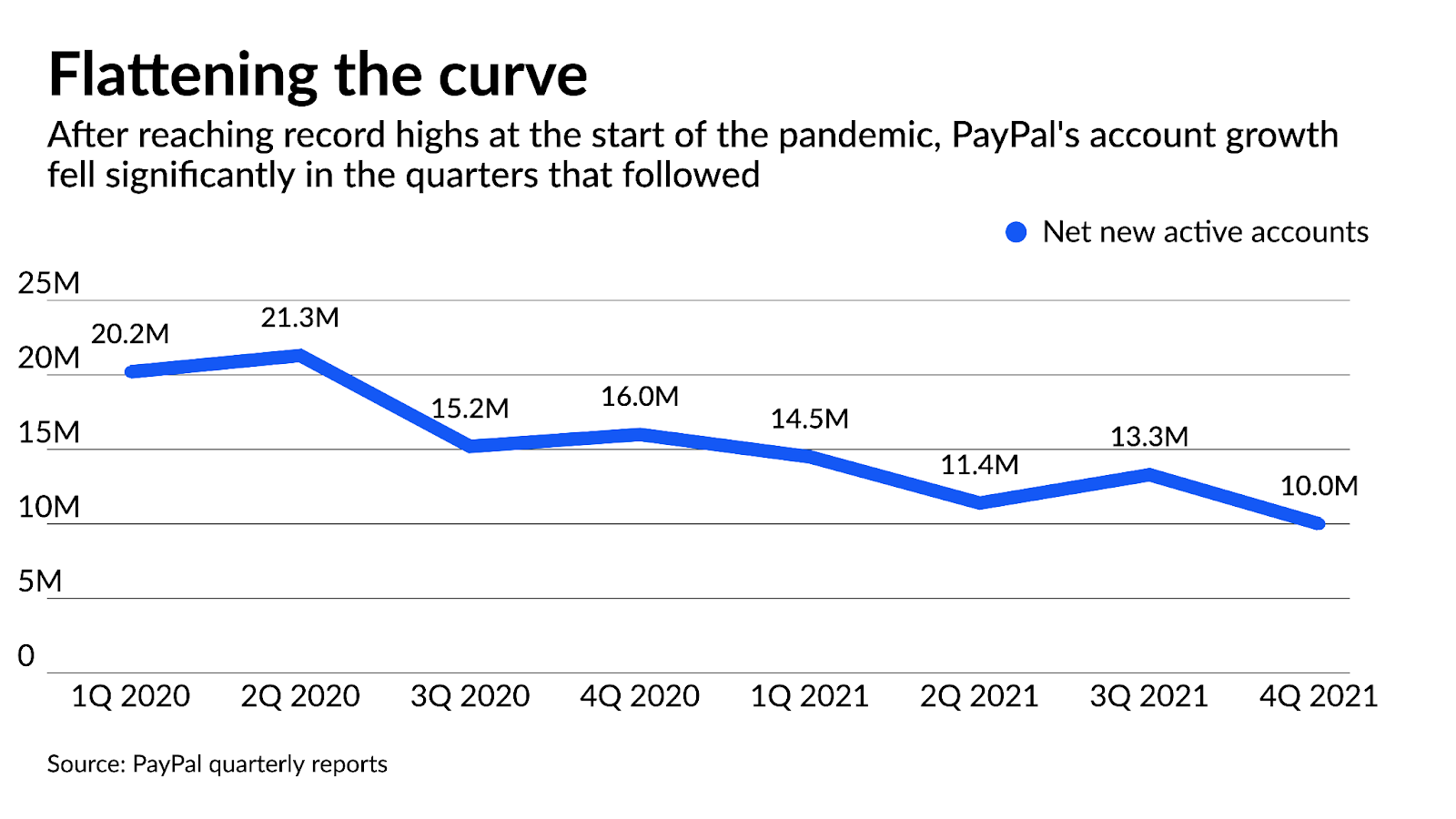

Combine that with the heights of ZIRP-drunk behaviour in 2021 and you will see real problems – even unintentional. An example of this would be PayPal’s admission that 4.5M fake accounts had been created to abuse their sign-up bonus schemes at the time. This admission was shortly followed by revised revenue projections, as they realised the huge outlay of capital was not going to yield the returns they had hoped.

Consider also how startup investments have been priced in recent years, with revenue multiples becoming the easy shorthand for valuation. In a 30x industry, as Fintech was at the peak, $1M in revenue became $30M in value – and due diligence wasn’t keeping up. Revenue was poorly scrutinized to begin with, and now it was having an outsized impact on fundraising.

Obvious Second Order Effect

Guess what happened once Founders realized that VCs were valuing startups using revenue multiples?

They started playing a game of Hungy Hungry Hippo with the goal of accumulating as much revenue as they could!

The magnification of value produced a powerful incentive for founders to exaggerate revenue with any trick imaginable… of which there are many: ‘round tripping’, reporting gross revenue rather than net, sketchy definitions of ‘booked revenue’, or treating discounts and refunds as expenses rather than contra-revenue events. For many, it became common practice to fudge revenue reporting (to varying degrees) in order to inflate performance and exaggerate potential.

When I joined Flexport as co-CEO in September 2022, I found a company lacking process and financial discipline, including numerous customer-facing issues that resulted in significant lost customers and a revenue forecasting model that was consistently providing overly optimistic outputs.

Unfortunately, conditions only worsened when the ZIRP-hangover began. After the leg-sweep of funding early in 2022, investors were briefly forgiving about slowed growth in the new environment but it didn’t last long. Today, founders are expected to live up to the kind of growth they had previously promised investors, without necessarily having the available venture capital dollars to afford it, all while angling more aggressively towards profit.

The crunch is real, and it will lead many founders to make bad decisions.

Challenges for investment due-diligence

A much discussed side-effect of the ZIRP-era coming to an end, with the collective tightening of belts in venture capital, is the resumed focus on proper due diligence with startup investments. This will include things like debt, leases and contracts, as well as the startup’s current and projected revenue.

This may already be catching out the lies from startups that exaggerate revenue to bump their valuation in a previous fundraising round, but it’s not always as clear cut. For this, we can look at the sordid history of GoMechanic, a startup caught in a revenue-faking scandal despite previously having sign-off on its accounts from Big Four accountants PwC and KPMG. The third time was the charm when EY finally managed to nail down where things were going wrong, including all kinds of accounting chicanery in a partially cash-based business.

This begs the question: how realistic is it for investors to catch-out revenue fraud for private companies, when there is so little in the way of enforced standards? Public companies are expected to adhere to GAAP (Generally Accepted Accounting Practices), but no such obligation exists for private companies. ASC 606 and IFRS 15 exist as revenue recognition standards for both private and public companies, but will continue to be ignored by startups for as long as they aren’t required by investors or properly scrutinised by board members.

For Fintech investors especially, this prompts the old debate about whether investors need to be experts in the industry in which they invest. If you are a partner at a financial services company (venture capital is really just a peculiar financing product), investing in financial services startups. should you not therefore have at least a minimum of financial literacy?

To go deeper down the rabbit-hole: there are questions about how much investors knew about some of these cases, before they were brought to light. When is it of interest to an investor to intervene, and go through the messy process of righting the ship, even when it may mean revising value downward for other investors, founders and employees? What if they just kept quiet, and let it be someone else’s problem?

VC doesn’t do real diligence because investors possess pseudo mystical beliefs about value creation in the asset that are nearly completely unmoored to data or scientific validity. You did a fair job demonstrating this via your post.

Increasingly, issues appear in the world of private company investment (and are amplified in the high risk/reward world of startups) which relate to a stark lack of transparency, accountability and regularity.

If venture capital firms invest in startups with the expectation that they will one day exit via IPO (and thus adhere to GAAP), why do they not require prospective investments and portfolio companies adhere to those standards from day one?

Startups are volatile in performance and unconventional by nature, making it impossible to standardise much about how they operate. In fact, I’d go so far as to say that conventional business wisdom is a plague on founders. However, much can be standardised about the ‘unsexy’ aspects of the fiduciary duty between founders and investors.

Founders are probably not jumping at the chance to apply accounting standards to their business. It is far easier, unless obliged otherwise, to sketch out an income statement with a degree of improvisation. A certain amount of poetic licence goes a long way for VCs, too.

However, it’s clear we are entering a new era for startups, with fresh scrutiny across the board – especially for Fintech. The world of startup investment is, slowly and painfully, moving towards greater levels of accountability.

We should also think carefully about the operating system of startup fundraising, and whether it really incentivises the best behavior and the best outcomes. I am a ‘techno-optimist’ in that I believe in the power of efficiently allocating capital to innovation… but that means real innovation, not monkey jpgs.

The success of AI is existential for venture capital

Imagine entering VC in 2020, full of enthusiasm about the unstoppable tide of technology. Your peers are impressed; it’s a prestigious industry that is perceived as commanding real influence over the future.

As you settle in, you put aside your personal thesis in favour of the firm’s strategy on crypto, micromobility, rapid delivery, creator economy, and web3. Each of those sectors are benefitting from venture capital enthusiasm and weaponised capital, driving prices through the roof. It’s an exciting time, though you’re not feeling as involved as you would like to be.

In fact, you’d quite like to make the case for investment in other industries; overlooked opportunities which offer larger ownership stakes and cleaner cap tables. It’s difficult to justify the change of strategy when the biggest markups are all coming from a few hot sectors, so you avoid the friction.

Capital is flowing into the asset class from LPs at an unprecedented rate. Rather than pressure to justify and properly diligence investments, you are pressed to ensure capital is deployed and opportunities aren’t missed. Access to hot deals and co-investment with the tier-1 firms is how you stay relevant to LPs. Success is now largely dependent on your relationships across the industry.

It creeps up on you that your colleagues have stopped talking about exits. TVPI looks phenomenal. There’s no rush for any portfolio company to go public. Now the conversation is about pricing and the appetite of downstream investors. Beyond that, it’s someone else’s problem.

For the first time, your spidey-senses start to tingle.

Early in 2022, concern ripples across the industry. Worries of recession, interest rates on the rise, and a weak public market that has lost interest in recent VC-backed IPOs. In simpler times, you would have papered over the cracks by highlighting fund resilience. Now, the idea fills you with dread. None of your portcos are growing much and auditors are on your tail to correct markups.

With surprising speed, the tables turn. An era of unprecedented growth and optimism comes to an end. Y Combinator writes the eulogy with an open letter to their portfolio companies. Venture-backed hypergrowth is shelved in favour of finding a path to profitability. The red-hot sectors which had promised game-changing returns are quietly scrubbed from websites and bios.

By Mid-2023, venture capital feels like a fever-dream. Many of the most exciting investments from 2020 and 2021 have imploded or recapitalised. Layoffs are the norm, even for many VC firms. Nobody in the arena wants to talk about why.

Fortunately, nobody has to dwell on the cause of the downturn for too long: exciting new tech from companies like OpenAI and Midjourney provides the perfect source of distraction. A whole new gold rush to sell to LPs.

The incredible possibilities offered by powerful, accessible AI models will spawn companies with growth potential not seen since the early years of Google and Amazon. It promises to easily turn-around a few years of poor performance for the venture asset class.

Of course, there are nay-sayers. Not the doomers who speak of an AI-driven apocalypse, at least they buy into the incredible scope of the technology. They are believers. The real problem are the cynics.

The cynic’s claim is that today’s “AI” is just an evolution of decades-long work on machine learning, neural networks and natural language processing. Yes, the hardware is a lot better, processing at scale is much easier, but fundamentally not a huge amount has changed. Models will be commoditised and commercial applications will favour incumbents who have data and distribution. It’s not the generational game-changer that venture capitalists claim.

Those who believe the hype (or those whose career depends on it) preach the gospel of salvation for an entire generation of managers. The narrative battleground is shifted to the conflict between these two groups, the doomers and the boomers, away from the cynics who offer nothing but grim reality.

Evangelism reaches new heights. Marc Andreessen who led the charge on the 2011 – 2022 bull run with his essay, “Why Software Is Eating the World“, proclaims even greater optimism with the publication of “Why AI Will Save the World“.

It gnaws at you. Do you really believe? Do the numbers make sense, or is venture capital back at its usual bullshit? Is it your responsibility to just blindly support this as an insider?

Worse, what if this fails too? The consequences for the venture asset class are difficult to contemplate.

At some point, you are sure the music is going to stop.

Until then, the only path you can see is to continue following your peers. As long as you are all doing the same thing, no failure can be pinned on you.

…Right?

Each day you scramble to find the hottest AI deals in your network and secure allocation. You keep making the same promises and assurances.

You lean into the identity, blend into the herd. Any sense of irony in wearing the uniform disappears. You begin to believe.